UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

Date

of Report (Date of earliest event reported):

|

October 22,

2008

|

AllianceBernstein

l.p.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

000-29961

|

13-4064930

|

|

(State

or other jurisdiction of incorporation or organization)

|

(Commission

File Number)

|

(I.R.S.

Employer Identification

Number)

|

|

1345

Avenue of the Americas, New York, New York

|

10105

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

Registrant’s

telephone number, including area code:

|

212-969-1000

|

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligations of the registrant under any of the following

provisions:

£ Written

communications pursuant to Rule 425 under the Securities Act (17 CFR

230.425)

£ Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR

240.14a-12)

£ Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR

240.14d-2(b))

£ Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR

240.13e-4(c))

|

Section

2.

|

Financial

Information

|

|

Item

2.02.

|

Results of Operations

and Financial Condition.

|

AllianceBernstein

L.P. (“AllianceBernstein”) is furnishing the news release it issued on October

22, 2008 concerning financial and operating results for the quarter ended

September 30, 2008 (“Release”). The Release is attached hereto as

Exhibit 99.01.

AllianceBernstein

is furnishing its Third Quarter 2008 Review, dated October 22, 2008

(“Review”). The Review is attached hereto as Exhibit

99.02.

AllianceBernstein

is furnishing a transcript of its conference call with analysts relating to the

Release and the Review (“Transcript”). The call took place on October

22, 2008. The Transcript is attached hereto as Exhibit

99.03.

|

Section

7.

|

Regulation

FD

|

|

Item

7.01.

|

Regulation FD

Disclosure.

|

AllianceBernstein

is furnishing the Release, which is attached hereto as Exhibit

99.01.

AllianceBernstein

is furnishing the Review, which is attached hereto as Exhibit

99.02.

AllianceBernstein

is furnishing the Transcript, which is attached hereto as Exhibit

99.03.

|

Section

9.

|

Financial Statements

and Exhibits

|

|

Item

9.01.

|

Financial Statements

and Exhibits.

|

|

|

(d)

|

Exhibits.

|

|

|

Release.

|

|

|

Review.

|

|

|

Transcript.

|

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant has

duly caused this report to be signed on its behalf by the undersigned thereunto

duly authorized.

|

AllianceBernstein

l.p.

|

||

|

Dated: October

23, 2008

|

By:

|

/s/

Robert H. Joseph, Jr.

|

|

Robert

H. Joseph, Jr.

Senior

Vice President and

Chief

Financial

Officer

|

||

EXHIBIT

99.01

|

|

|

Philip

Talamo, Investor Relations

212.969.2383

ir@alliancebernstein.com

|

John

Meyers, Media

212.969.2301

pr@alliancebernstein.com

|

News

Release

AllianceBernstein

Holding L.P. Announces Third Quarter Diluted Net Income of $0.73 per

Unit;

Declares

a $0.60 per Unit Cash Distribution, which Excludes Insurance Recoveries of $0.13

per Unit

New

York, NY, October 22, 2008 – AllianceBernstein

Holding L.P. (“AllianceBernstein Holding”) (NYSE: AB) and

AllianceBernstein L.P. (“AllianceBernstein”) today reported financial and

operating results for the quarter ended September 30, 2008.

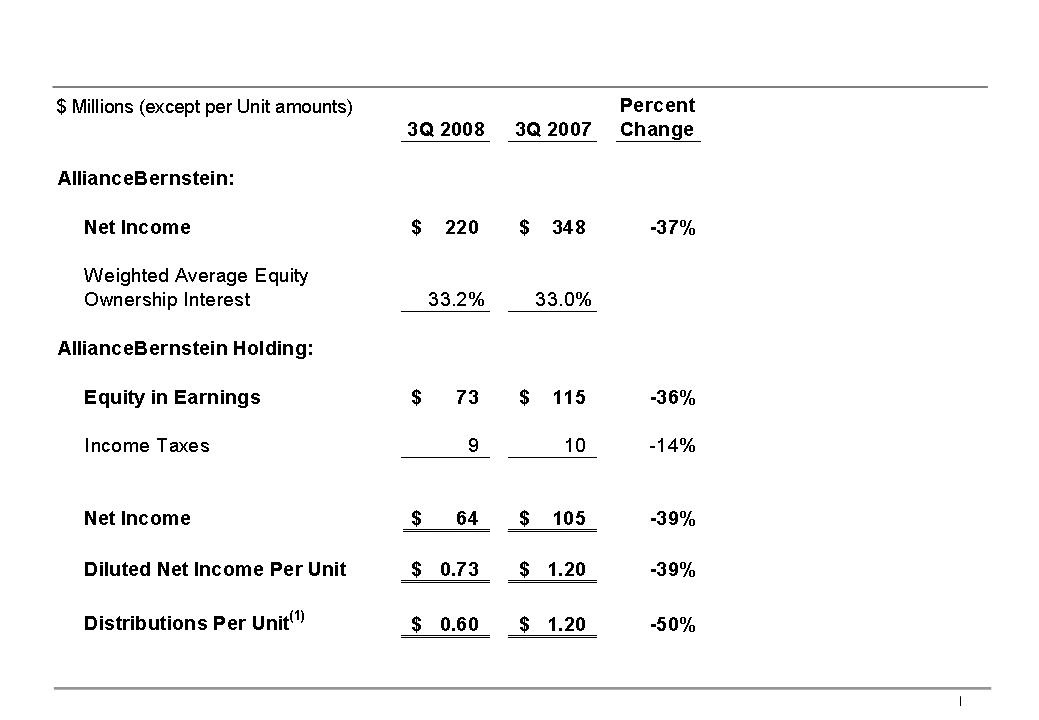

AllianceBernstein

Holding (The Publicly Traded Partnership):

|

·

|

Diluted net income per

Unit for the quarter ended September 30,

2008 was $0.73, a decrease of 39% from $1.20 for the same

period in 2007.

|

|

·

|

Distribution per Unit

for the third quarter of 2008 will be $0.60, a decrease of 50% from $1.20

for the same period in 2007. The distribution is payable on

November 13, 2008 to holders of record of AllianceBernstein Holding Units

at the close of business on November 3,

2008.

|

During

the third quarter of 2008, AllianceBernstein recorded

approximately $35.3 million in insurance recoveries relating to payments made

for a class action claims processing error. A reserve of $56.0

million was established in the fourth quarter of 2006 for this

error. AllianceBernstein Holding’s fourth quarter 2006 cash

distribution was based on net income before this charge. Accordingly,

these recoveries were not included in the per Unit cash distribution for the

current quarter.

AllianceBernstein

(The Operating Partnership):

|

·

|

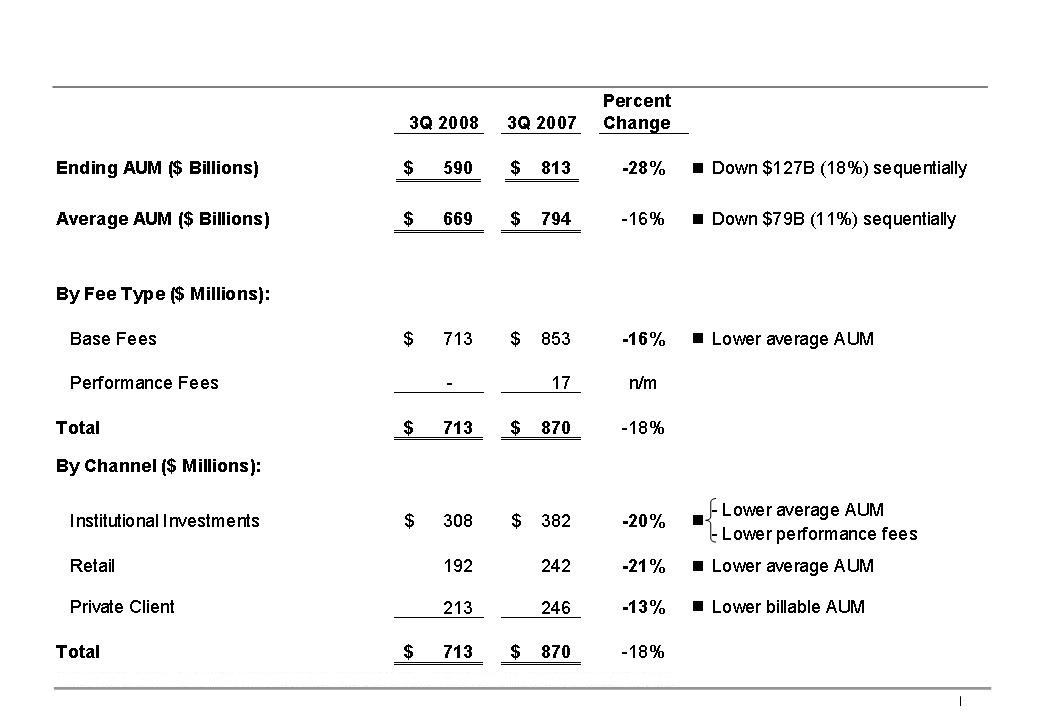

Assets Under Management

(AUM) at September 30, 2008 were $590 billion, a 28% decrease from

a year ago, due to net outflows and substantial market

depreciation.

|

|

·

|

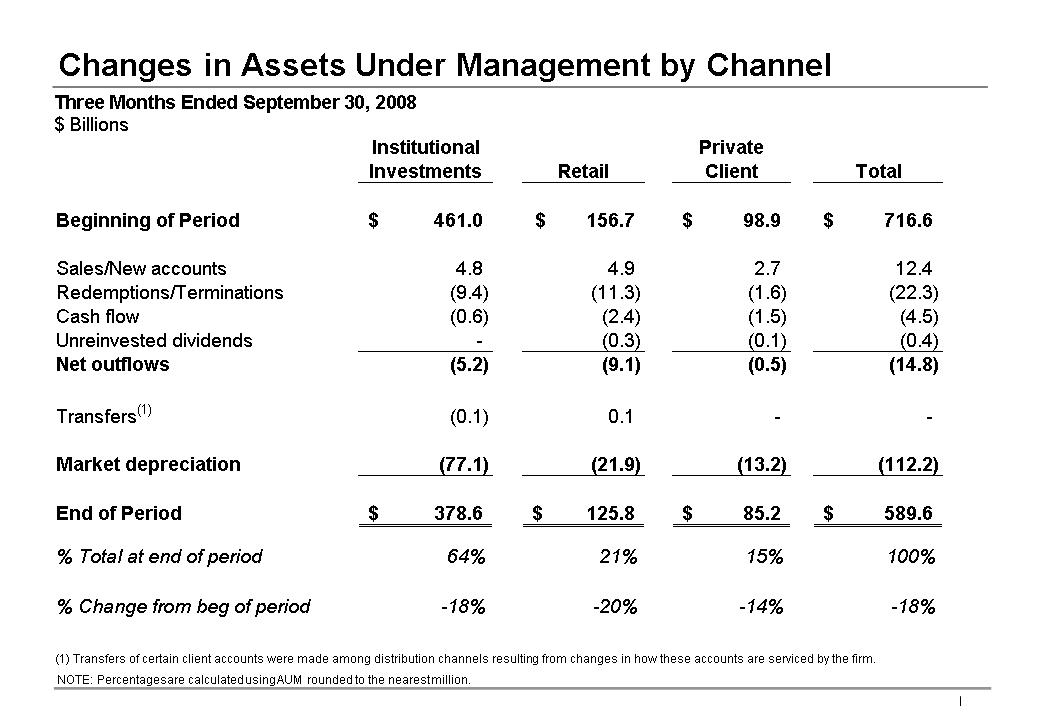

Net outflows for the three months

ended September 30, 2008 were $14.8 billion, consisting of Retail

net outflows of $9.1 billion, Institutional Investments net outflows of

$5.2 billion and Private Client net outflows of $0.5

billion.

|

|

·

|

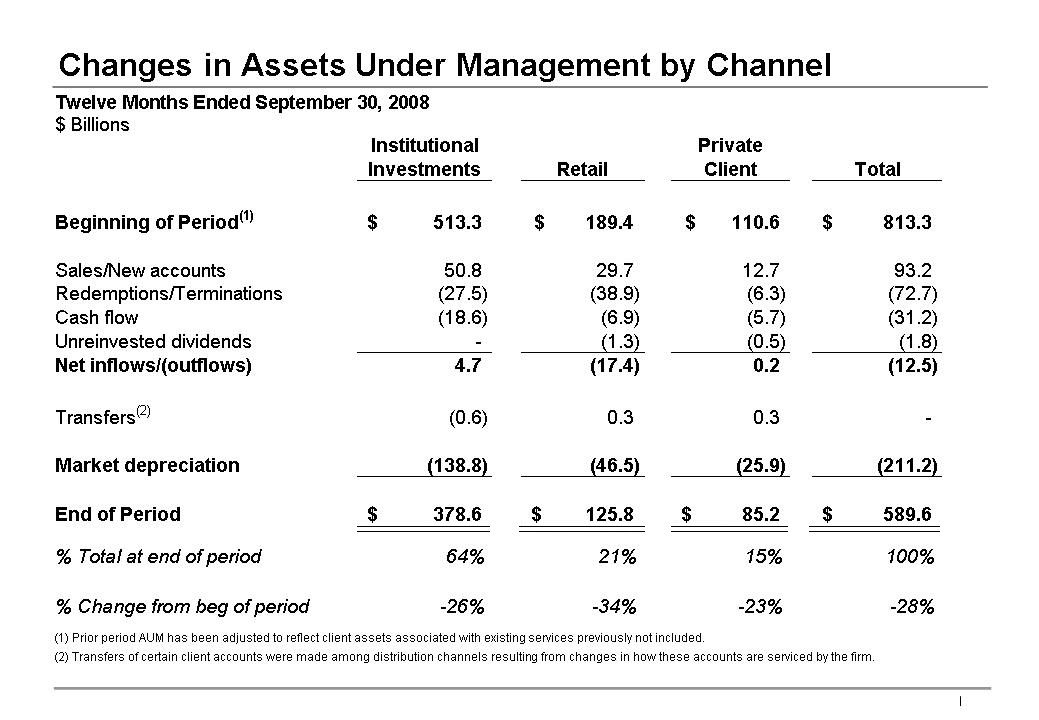

Net outflows for the twelve

months ended September 30, 2008 were $12.5 billion, consisting of

Retail net outflows of $17.4 billion, Institutional Investments net

inflows of $4.7 billion and Private Client net inflows of $0.2

billion.

|

“In the

third quarter of 2008, exceptionally turbulent capital market conditions led to

sharply negative absolute investment returns in most of our investment services.

Relative performance suffered as well, owing to our exposure to sectors directly

affected by the global financial crisis. Our substantial weighting of non-US

investments added still more downward pressure to results, as the US dollar

strengthened considerably during the quarter. While investment returns are

clearly disappointing, we continue to believe that client portfolios are

positioned to weather the current storm and recover strongly after it lifts.

Some of our best periods of absolute and relative returns have occurred in the

aftermath of prior bouts of market turbulence, and we anticipate that this

pattern will repeat itself in the current episode” said Lewis Sanders, Chairman

and Chief Executive Officer.

“The

firm’s organic growth remained negative in the third quarter, with outflows

accelerating versus the second quarter of 2008 in Retail and Institutional

Investments channels, while Private Client outflows remained

modest. Retail outflows were driven by both significantly slower

sales and a marked increase in redemptions. Institutional Investments outflows

were primarily a function of sharply lower sales, rather than higher account

terminations and the backlog of new but not yet funded institutional mandates

declined slightly to $14 billion. If history is a guide, the firm’s organic

growth will likely remain under considerable pressure until market conditions

improve.

“Our

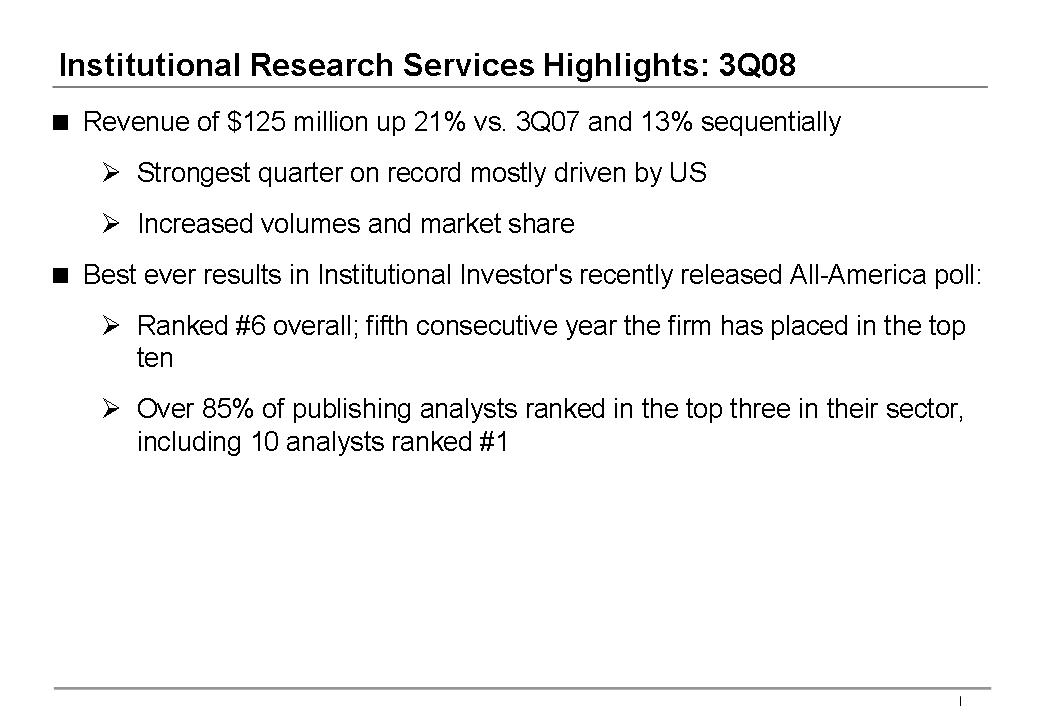

institutional research services unit continued to perform very well, with

revenues in the third quarter up 21% year-over-year and 13% sequentially,

benefiting from strong volume growth and market share gains, especially in the

US. The firm continued to improve its competitive standing in research

quality. We ranked 6th in

Institutional Investor's recently released All-America poll and ten of our

analysts ranked #1 in their sector, the strongest showing in our

history.

“The

firm’s financial results were quite weak in the third quarter, as the

precipitous decline in the global capital markets impacted assets under

management and related fee revenue. The revenue decline was exacerbated by

losses of $123 million on investments related to employee deferred compensation,

which, net of lower compensation expenses and taxes, reduced reported earnings

by about $0.24 per Unit. Despite aggressive expense management, operating margin

fell year-over-year by 410 basis points to 28.8%. The margin decline was

moderated by insurance recoveries of approximately $35.3 million ($0.13 per

Unit) relating to a class action claims processing error for which a $56.0

million reserve was established in the fourth quarter of 2006. As

cash distributions to Unitholders were not reduced when the reserves were

established, the insurance recoveries are not included in distributable income

in the current quarter.

www.alliancebernstein.com

2 of

10

“With

assets under management now far below expectations, the company is moving to

reset its expense base and capital outlays to an appropriate level. The highly

variable nature of our cost structure will be helpful in accomplishing this

mission. However, a reduction in headcount, much of which will be implemented in

this year’s fourth quarter, is unavoidable and will result in a charge against

earnings, the size of which has not been determined. Additionally, capital

spending plans have been reduced to a level below depreciation and amortization.

These actions notwithstanding, we will be moving ahead on the new business

initiatives that we believe are most important to the firm’s future

growth.

“Of equal

importance, the firm’s solid financial foundation and limited use of its balance

sheet for purposes other than normal working capital requirements position us

well to navigate through this difficult period.

“These

are tough times, to be sure. In such times, having a single-minded

focus on producing superior investment returns and delivering world class

service to our clients is evermore important and remains the number one priority

of all AllianceBernstein employees,” concluded Mr. Sanders.

CONFERENCE

CALL INFORMATION RELATING TO THIRD QUARTER 2008 RESULTS

OCTOBER

22, 2008 AT 5:00 P.M. (Eastern Daylight Time)

AllianceBernstein’s

management will review third quarter 2008 financial and operating results on

Wednesday, October 22, 2008, during a conference call beginning at 5:00 p.m.

(EDT),

following the release of its financial results after the close of the New York

Stock Exchange. The conference call will be hosted by Lewis A.

Sanders, Chairman and Chief Executive Officer, and Gerald M. Lieberman,

President and Chief Operating Officer.

Parties

may access the conference call by either webcast or telephone:

|

1.

|

To

listen by webcast, please visit AllianceBernstein’s Investor Relations

website at http://ir.alliancebernstein.com/investorrelations

at least 15 minutes prior to the call to download and install any

necessary audio software.

|

|

2.

|

To

listen by telephone, please dial (866) 556-2265 in the U.S. or (973)

935-8521 outside the U.S., 10 minutes before the 5:00 p.m. (EDT)

scheduled start time. The conference ID# is

68115800.

|

The

presentation that will be reviewed during the conference call will be made

available on AllianceBernstein’s Investor Relations website shortly after the

release of third quarter 2008 financial results on October 22,

2008.

An audio

replay of the conference call will be made available beginning at approximately

7:00 p.m. (EDT) on October 22, 2008 and will be available for one week. To

access the audio replay, please call (800) 642-1687 from the U.S., or outside

the U.S. call (706) 645-9291, and provide conference ID#

68115800. The replay will also be available via webcast on

AllianceBernstein’s website for one week.

www.alliancebernstein.com

3 of

10

About

AllianceBernstein

AllianceBernstein

is a leading global investment management firm that offers high-quality research

and diversified investment services to institutional clients, individuals and

private clients in major markets around the world. AllianceBernstein

employs more than 500 investment professionals with expertise in growth

equities, value equities, fixed income securities, blend strategies and

alternative investments and, through its subsidiaries and joint ventures,

operates in more than 20 countries. AllianceBernstein’s research

disciplines include fundamental research, quantitative research, economic

research and currency forecasting capabilities. Through its

integrated global platform, AllianceBernstein is well-positioned to tailor

investment solutions for its clients. AllianceBernstein also offers independent

research, portfolio strategy and brokerage-related services to institutional

investors.

At

September 30, 2008, AllianceBernstein Holding L.P. (“Holding”) owned

approximately 33.6% of the issued and outstanding AllianceBernstein

Units. AXA Financial was the beneficial owner of approximately 62.6%

of the AllianceBernstein Units at September 30, 2008 (including those held

indirectly through its ownership of approximately 1.6% of the issued and

outstanding Holding Units) which, including the general partnership interests in

AllianceBernstein and Holding, represent an approximate 63.0% economic interest

in AllianceBernstein. AXA Financial is a wholly-owned subsidiary of

AXA, one of the largest global financial services organizations.

Cautions

regarding Forward-Looking Statements

Certain

statements provided by management in this news release are “forward-looking

statements” within the meaning of the Private Securities Litigation Reform Act

of 1995. Such forward-looking statements are subject to risks, uncertainties,

and other factors that could cause actual results to differ materially from

future results expressed or implied by such forward-looking statements. The most

significant of these factors include, but are not limited to, the following: the

performance of financial markets, the investment performance of sponsored

investment products and separately managed accounts, general economic

conditions, future acquisitions, competitive conditions, and government

regulations, including changes in tax regulations and rates and the manner in

which the earnings of publicly traded partnerships are taxed. We caution readers

to carefully consider such factors. Further, such forward-looking statements

speak only as of the date on which such statements are made; we undertake no

obligation to update any forward-looking statements to reflect events or

circumstances after the date of such statements. For further information

regarding these forward-looking statements and the factors that could cause

actual results to differ, see “Risk Factors” in Part I, Item 1A of

our Form 10-K for the year ended December 31, 2007 and Part II, Item 1A of our

Form 10-Q for the quarter ended June 30, 2008. Any or all of the forward-looking

statements that we make in this news release, Form 10-K, Form 10-Q, other

documents we file with or furnish to the SEC, or any other public statements we

issue, may turn out to be wrong. It is important to remember that other factors

besides those listed in “Risk Factors” and those listed above and below could

also adversely affect our revenues, financial condition, results of operations,

and business prospects.

www.alliancebernstein.com

4 of

10

The

forward-looking statements referred to in the preceding paragraph include

statements regarding:

|

|

·

|

Our

anticipation that the historical pattern of some of our best absolute and

relative returns following bouts of market turbulence will repeat itself

in the current episode, and our confidence

that the actions we are taking will position us to take advantage of a

recovery for our clients and for the firm which history tells us will

arrive sooner and be stronger than generally expected: Historical

performance is not necessarily indicative of future results or market

movements. The actual performance of the capital markets and

other factors beyond our control will affect our investment success for

clients and asset flows.

|

|

|

·

|

Our backlog

of new institutional mandates not yet funded: Before they are

funded, institutional mandates do not represent legally binding

commitments to fund and, accordingly, the possibility exists that not all

mandates will be funded in the amounts and at the times we currently

anticipate.

|

|

|

·

|

The firm’s

solid financial foundation positioning it well to navigate through this

difficult period: Our solid financial foundation is

dependent on our cash flow from operations, which is subject to the

performance of the capital markets and other factors beyond our

control.

|

www.alliancebernstein.com

5 of

10

ALLIANCEBERNSTEIN

L.P.

(THE

OPERATING PARTNERSHIP)

SUMMARY

CONSOLIDATED STATEMENTS OF INCOME

SEPTEMBER

30, 2008

(unaudited,

$ thousands)

|

Three Months Ended

|

||||||||

|

9/30/08

|

9/30/07

|

|||||||

|

Revenues:

|

||||||||

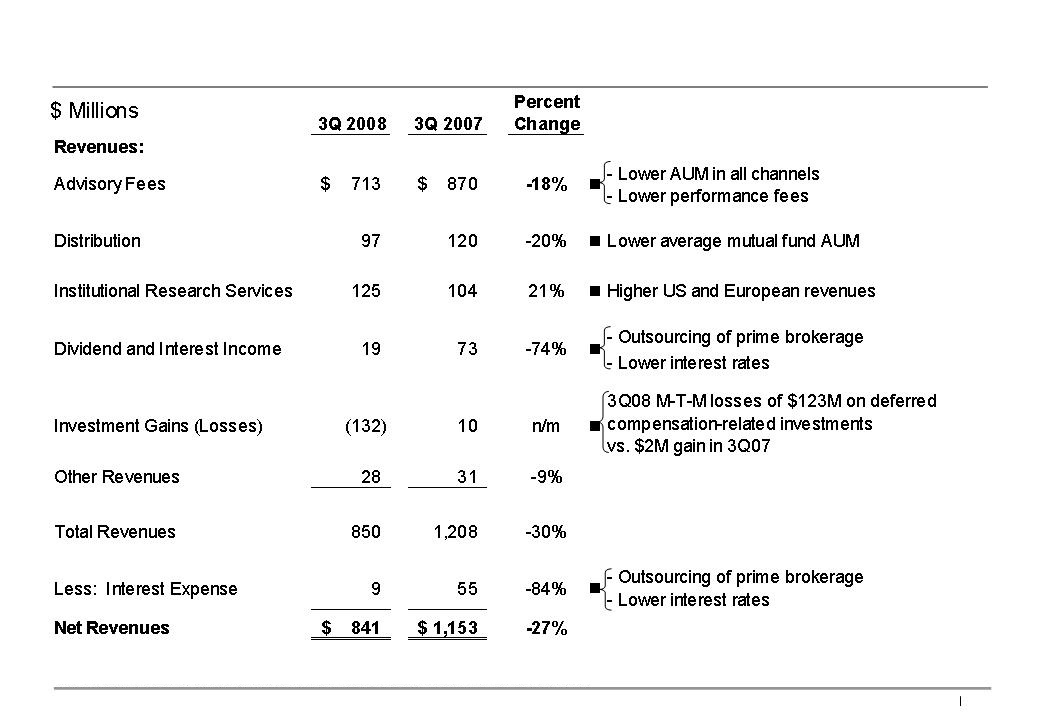

|

Investment

Advisory & Services Fees

|

$ | 713,229 | $ | 870,282 | ||||

|

Distribution

Revenues

|

96,711 | 120,289 | ||||||

|

Institutional

Research Services

|

124,854 | 103,552 | ||||||

|

Dividend

and Interest Income

|

18,937 | 72,665 | ||||||

|

Investment

Gains (Losses)

|

(131,920 | ) | 10,200 | |||||

|

Other

Revenues

|

28,230 | 30,856 | ||||||

|

Total

Revenues

|

850,041 | 1,207,844 | ||||||

|

Less:

Interest Expense

|

9,050 | 55,022 | ||||||

|

Net

Revenues

|

840,991 | 1,152,822 | ||||||

|

Expenses:

|

||||||||

|

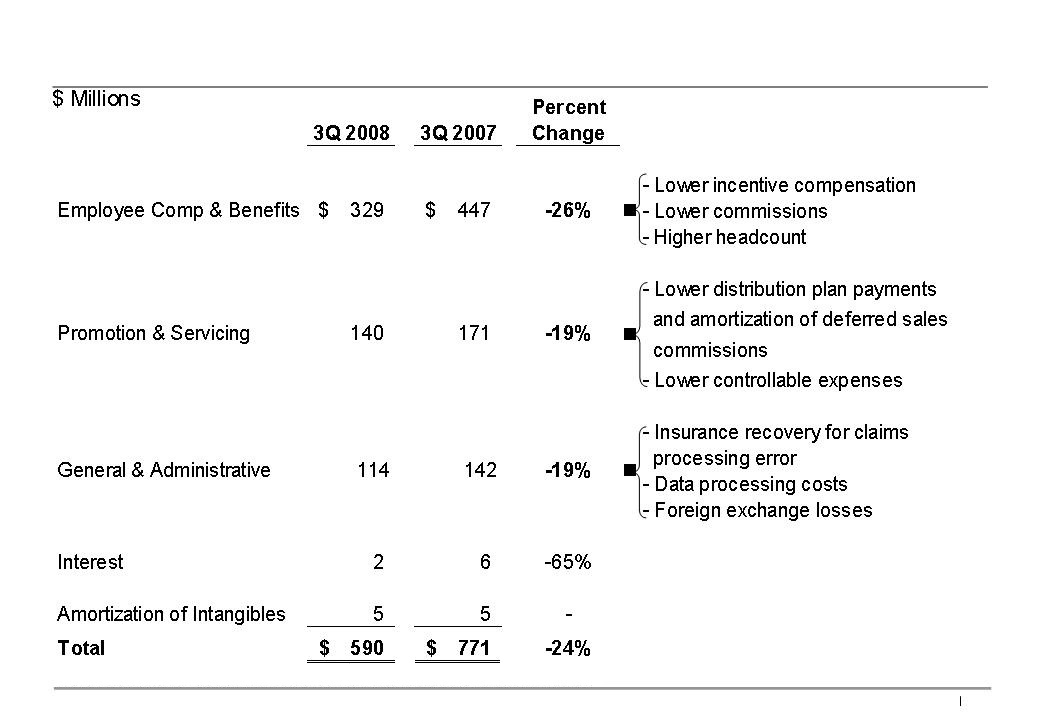

Employee

Compensation & Benefits

|

328,614 | 446,938 | ||||||

|

Promotion

& Servicing:

|

||||||||

|

Distribution

Plan Payments

|

69,994 | 86,230 | ||||||

|

Amortization

of Deferred Sales Commissions

|

19,324 | 23,739 | ||||||

|

Other

|

50,013 | 61,192 | ||||||

|

General

& Administrative

|

114,333 | 141,894 | ||||||

|

Interest

on Borrowings

|

2,117 | 5,965 | ||||||

|

Amortization

of Intangible Assets

|

5,179 | 5,179 | ||||||

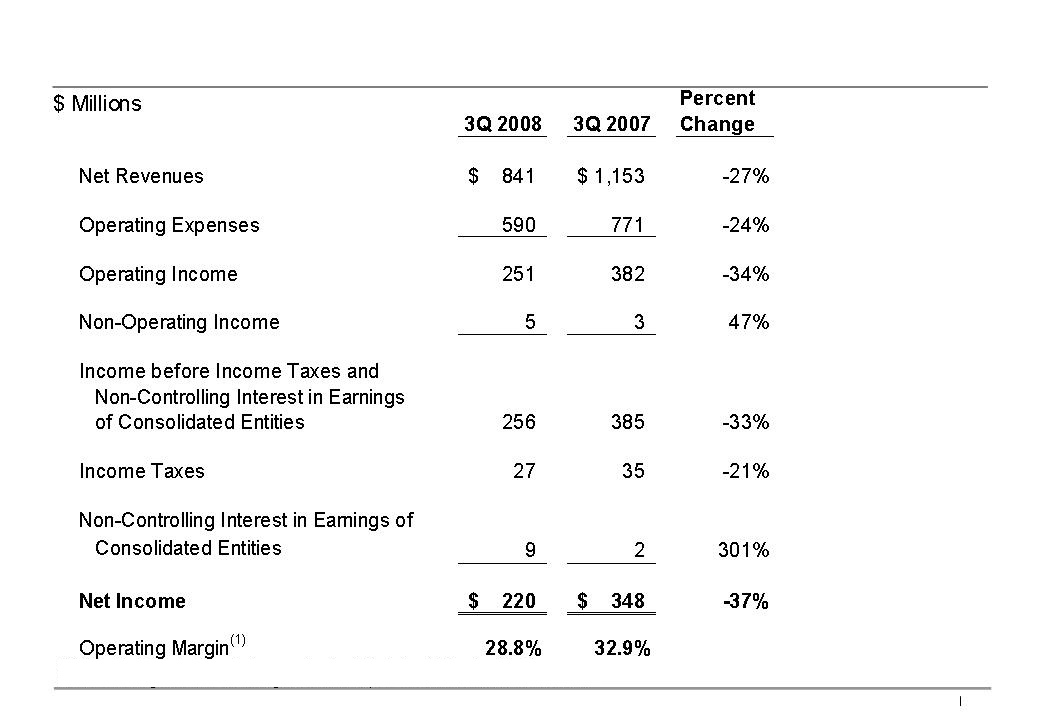

| 589,574 | 771,137 | |||||||

|

Operating

Income

|

251,417 | 381,685 | ||||||

|

Non-Operating

Income

|

4,921 | 3,353 | ||||||

|

Income

before Income Taxes and Non-Controlling

|

||||||||

|

Interest

in Earnings of Consolidated Entities

|

256,338 | 385,038 | ||||||

|

Income

Taxes

|

27,258 | 34,574 | ||||||

|

Non-Controlling

Interest in Earnings of Consolidated Entities,

|

||||||||

|

Net

of Taxes

|

9,551 | 2,382 | ||||||

|

NET

INCOME

|

$ | 219,529 | $ | 348,082 | ||||

|

Operating

Margin(1)

|

28.8 | % | 32.9 | % | ||||

www.alliancebernstein.com

6 of

10

ALLIANCEBERNSTEIN HOLDING

L.P.

(THE

PUBLICLY TRADED PARTNERSHIP)

SUMMARY

STATEMENTS OF INCOME

(unaudited,

$ thousands except per unit amounts)

|

Three Months Ended

|

||||||||

|

9/30/08

|

9/30/07

|

|||||||

|

Equity

in Earnings of Operating Partnership

|

$ | 72,936 | $ | 114,856 | ||||

|

Income

Taxes

|

8,575 | 10,028 | ||||||

|

NET

INCOME

|

64,361 | 104,828 | ||||||

|

Additional

Equity in Earnings of Operating Partnership(1)

|

251 | 1,243 | ||||||

|

NET

INCOME - Diluted(2)

|

$ | 64,612 | $ | 106,071 | ||||

|

DILUTED

NET INCOME PER UNIT

|

$ | 0.73 | $ | 1.20 | ||||

|

DISTRIBUTION

PER UNIT(3)

|

$ | 0.60 | $ | 1.20 | ||||

(1) To

reflect higher ownership in the Operating Partnership resulting from application

of the treasury stock method to outstanding options.

(2) For

calculation of Diluted Net Income per Unit.

(3)

Excludes insurance recoveries related to class action claims processing

error.

ALLIANCEBERNSTEIN L.P. AND ALLIANCEBERNSTEIN HOLDING

L.P.

UNITS

OUTSTANDING AND WEIGHTED AVERAGE UNITS OUTSTANDING

SEPTEMBER

30, 2008

|

Weighted

Average Units Three Months

Ended

|

||||||||||||

|

Period

End

|

||||||||||||

|

Units

|

Basic

|

Diluted

|

||||||||||

|

AllianceBernstein

L.P.

|

260,989,769 | 260,975,837 | 261,490,610 | |||||||||

|

AllianceBernstein

Holding

|

87,595,926 | 87,581,994 | 88,096,767 | |||||||||

www.alliancebernstein.com

7 of

10

ALLIANCEBERNSTEIN L.P.

ASSETS

UNDER MANAGEMENT

THREE

MONTHS ENDED SEPTEMBER 30, 2008

($

billions)

|

Institutional

Investments

|

Retail

|

Private

Client

|

Total

|

|||||||||||||

|

Beginning

of Period

|

$ | 461.0 | $ | 156.7 | $ | 98.9 | $ | 716.6 | ||||||||

|

Sales/New

accounts

|

4.8 | 4.9 | 2.7 | 12.4 | ||||||||||||

|

Redemptions/Terminations

|

(9.4 | ) | (11.3 | ) | (1.6 | ) | (22.3 | ) | ||||||||

|

Cash

flow

|

(0.6 | ) | (2.4 | ) | (1.5 | ) | (4.5 | ) | ||||||||

|

Unreinvested

dividends

|

- | (0.3 | ) | (0.1 | ) | (0.4 | ) | |||||||||

|

Net

outflows

|

(5.2 | ) | (9.1 | ) | (0.5 | ) | (14.8 | ) | ||||||||

|

Transfers(1)

|

(0.1 | ) | 0.1 | - | - | |||||||||||

|

Market

depreciation

|

(77.1 | ) | (21.9 | ) | (13.2 | ) | (112.2 | ) | ||||||||

|

End

of Period

|

$ | 378.6 | $ | 125.8 | $ | 85.2 | $ | 589.6 | ||||||||

(1)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the

firm.

ALLIANCEBERNSTEIN L.P.

ASSETS

UNDER MANAGEMENT

TWELVE

MONTHS ENDED SEPTEMBER 30, 2008

($

billions)

|

Institutional

Investments

|

Retail

|

Private

Client

|

Total

|

|||||||||||||

|

Beginning

of Period(1)

|

$ | 513.3 | $ | 189.4 | $ | 110.6 | $ | 813.3 | ||||||||

|

Sales/New

accounts

|

50.8 | 29.7 | 12.7 | 93.2 | ||||||||||||

|

Redemptions/Terminations

|

(27.5 | ) | (38.9 | ) | (6.3 | ) | (72.7 | ) | ||||||||

|

Cash

flow

|

(18.6 | ) | (6.9 | ) | (5.7 | ) | (31.2 | ) | ||||||||

|

Unreinvested

dividends

|

- | (1.3 | ) | (0.5 | ) | (1.8 | ) | |||||||||

|

Net

inflows/(outflows)

|

4.7 | (17.4 | ) | 0.2 | (12.5 | ) | ||||||||||

|

Transfers(2)

|

(0.6 | ) | 0.3 | 0.3 | - | |||||||||||

|

Market

depreciation

|

(138.8 | ) | (46.5 | ) | (25.9 | ) | (211.2 | ) | ||||||||

|

End

of Period

|

$ | 378.6 | $ | 125.8 | $ | 85.2 | $ | 589.6 | ||||||||

(1) Prior

period AUM has been adjusted to reflect client assets associated with existing

services previously not included.

(2)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the

firm.

www.alliancebernstein.com

8 of

10

ALLIANCEBERNSTEIN L.P.

ASSETS

UNDER MANAGEMENT

BY

INVESTMENT SERVICE

AT

SEPTEMBER 30, 2008

($

billions)

|

Institutional Investments

|

Retail

|

Private Client

|

Total

|

|||||||||||||

|

Equity:

|

||||||||||||||||

|

Value

|

||||||||||||||||

|

U.S.

|

$ | 33.1 | $ | 21.4 | $ | 17.7 | $ | 72.2 | ||||||||

|

Global

& International

|

127.6 | 35.8 | 16.5 | 179.9 | ||||||||||||

| 160.7 | 57.2 | 34.2 | 252.1 | |||||||||||||

|

Growth

|

||||||||||||||||

|

U.S.

|

21.8 | 16.3 | 11.6 | 49.7 | ||||||||||||

|

Global

& International

|

58.9 | 14.8 | 8.2 | 81.9 | ||||||||||||

| 80.7 | 31.1 | 19.8 | 131.6 | |||||||||||||

|

Total

Equity

|

241.4 | 88.3 | 54.0 | 383.7 | ||||||||||||

|

Fixed

Income:

|

||||||||||||||||

|

U.S.

|

67.2 | 9.2 | 30.4 | 106.8 | ||||||||||||

|

Global

& International

|

54.7 | 24.8 | 0.8 | 80.3 | ||||||||||||

| 121.9 | 34.0 | 31.2 | 187.1 | |||||||||||||

|

Other(1)

|

||||||||||||||||

|

U.S.

|

8.4 | 3.5 | - | 11.9 | ||||||||||||

|

Global

& International

|

6.9 | - | - | 6.9 | ||||||||||||

| 15.3 | 3.5 | - | 18.8 | |||||||||||||

|

Total:

|

||||||||||||||||

|

U.S.

|

130.5 | 50.4 | 59.7 | 240.6 | ||||||||||||

|

Global

& International

|

248.1 | 75.4 | 25.5 | 349.0 | ||||||||||||

| $ | 378.6 | $ | 125.8 | $ | 85.2 | $ | 589.6 | |||||||||

(1)

Includes Index, Structured and Asset Allocation services.

www.alliancebernstein.com

9 of

10

ALLIANCEBERNSTEIN L.P.

ASSETS

UNDER MANAGEMENT

($

billions)

|

Three Month Period

|

Twelve Month Period

|

|||||||||||||||

|

09/30/08

|

9/30/2007(1)

|

09/30/08

|

9/30/2007(1)

|

|||||||||||||

|

Ending

Assets Under Management

|

$ | 589.6 | $ | 813.3 | $ | 589.6 | $ | 813.3 | ||||||||

|

Average

Assets Under Management

|

$ | 669.2 | $ | 794.1 | $ | 746.7 | $ | 745.2 | ||||||||

(1) Prior

period AUM has been adjusted to reflect client assets associated with existing

services previously not included.

ALLIANCEBERNSTEIN L.P.

ASSETS

UNDER MANAGEMENT

BY

CLIENT DOMICILE

AT

SEPTEMBER 30, 2008

($

billions)

|

Institutional Investments

|

Retail

|

Private Client

|

Total

|

|||||||||||||

|

U.

S. Clients

|

$ | 177.4 | $ | 97.7 | $ | 82.5 | $ | 357.6 | ||||||||

|

Non-U.S.

Clients

|

201.2 | 28.1 | 2.7 | 232.0 | ||||||||||||

|

Total

|

$ | 378.6 | $ | 125.8 | $ | 85.2 | $ | 589.6 | ||||||||

www.alliancebernstein.com

10 of

10

EXHIBIT 99.02

AllianceBernstein

Third

Quarter 2008 Review

Third

Quarter 2008 Review

Gerald

M. Lieberman

President & Chief Operating Officer

President & Chief Operating Officer

Lewis

A. Sanders

Chairman & Chief Executive Officer

Chairman & Chief Executive Officer

Any

forecasts in this material may not be realized. Information or opinions should

not be construed as investment advice.

October

22, 2008

AllianceBernstein

2

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Cautions

regarding Forward-Looking Statements

Certain

statements provided by management in this presentation are “forward-looking

statements” within the meaning of the Private Securities

Litigation Reform Act of 1995. Such forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results

to differ materially from future results expressed or implied by such forward-looking statements. The most significant of these factors include, but

are not limited to, the following: the performance of financial markets, the investment performance of sponsored investment products and

separately managed accounts, general economic conditions, future acquisitions, competitive conditions, and government regulations, including

changes in tax regulations and rates and the manner in which the earnings of publicly traded partnerships are taxed. We caution readers to

carefully consider such factors. Further, such forward-looking statements speak only as of the date on which such statements are made; we

undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements. For further

information regarding these forward-looking statements and the factors that could cause actual results to differ, see “Risk Factors” in Part I, Item

1A of our Form 10-K for the year ended December 31, 2007 and Part II, Item 1A of our Form 10-Q for the quarter ended June 30, 2008. Any or all

of the forward-looking statements that we make in this presentation, Form 10-K, Form 10-Q, other documents we file with or furnish to the SEC, or

any other public statements we issue, may turn out to be wrong. It is important to remember that other factors besides those listed in “Risk Factors”

and those listed above and below could also adversely affect our revenues, financial condition, results of operations, and business prospects.

Litigation Reform Act of 1995. Such forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results

to differ materially from future results expressed or implied by such forward-looking statements. The most significant of these factors include, but

are not limited to, the following: the performance of financial markets, the investment performance of sponsored investment products and

separately managed accounts, general economic conditions, future acquisitions, competitive conditions, and government regulations, including

changes in tax regulations and rates and the manner in which the earnings of publicly traded partnerships are taxed. We caution readers to

carefully consider such factors. Further, such forward-looking statements speak only as of the date on which such statements are made; we

undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements. For further

information regarding these forward-looking statements and the factors that could cause actual results to differ, see “Risk Factors” in Part I, Item

1A of our Form 10-K for the year ended December 31, 2007 and Part II, Item 1A of our Form 10-Q for the quarter ended June 30, 2008. Any or all

of the forward-looking statements that we make in this presentation, Form 10-K, Form 10-Q, other documents we file with or furnish to the SEC, or

any other public statements we issue, may turn out to be wrong. It is important to remember that other factors besides those listed in “Risk Factors”

and those listed above and below could also adversely affect our revenues, financial condition, results of operations, and business prospects.

The

forward-looking statements referred to in the preceding paragraph include

statements regarding:

= Our

anticipation that the historical pattern of some of our best absolute and

relative returns following bouts of market turbulence

will repeat itself in the current episode, and our confidence that the actions we are taking will position us to take advantage of a

recovery for our clients and for the firm which history tells us will arrive sooner and be stronger than generally expected:

Historical performance is not necessarily indicative of future results or market movements. The actual performance of the capital markets

and other factors beyond our control will affect our investment success for clients and asset flows.

will repeat itself in the current episode, and our confidence that the actions we are taking will position us to take advantage of a

recovery for our clients and for the firm which history tells us will arrive sooner and be stronger than generally expected:

Historical performance is not necessarily indicative of future results or market movements. The actual performance of the capital markets

and other factors beyond our control will affect our investment success for clients and asset flows.

= Our

backlog of new institutional mandates not yet funded: Before they are

funded, institutional mandates do not represent legally

binding commitments to fund and, accordingly, the possibility exists that not all mandates will be funded in the amounts and at the times we

currently anticipate.

binding commitments to fund and, accordingly, the possibility exists that not all mandates will be funded in the amounts and at the times we

currently anticipate.

= The

firm’s solid financial foundation positioning it well to navigate through this

difficult period: Our solid financial

foundation is

dependent on our cash flow from operations, which is subject to the performance of the capital markets and other factors beyond our

control.

dependent on our cash flow from operations, which is subject to the performance of the capital markets and other factors beyond our

control.

= Our

hope that we will recover an additional portion of the $56.0 million claim

processing error-related charge: Our ability to

recover

more of this cost depends on the availability of funds from the related class-action settlements fund, the amount of which is not yet known.

more of this cost depends on the availability of funds from the related class-action settlements fund, the amount of which is not yet known.

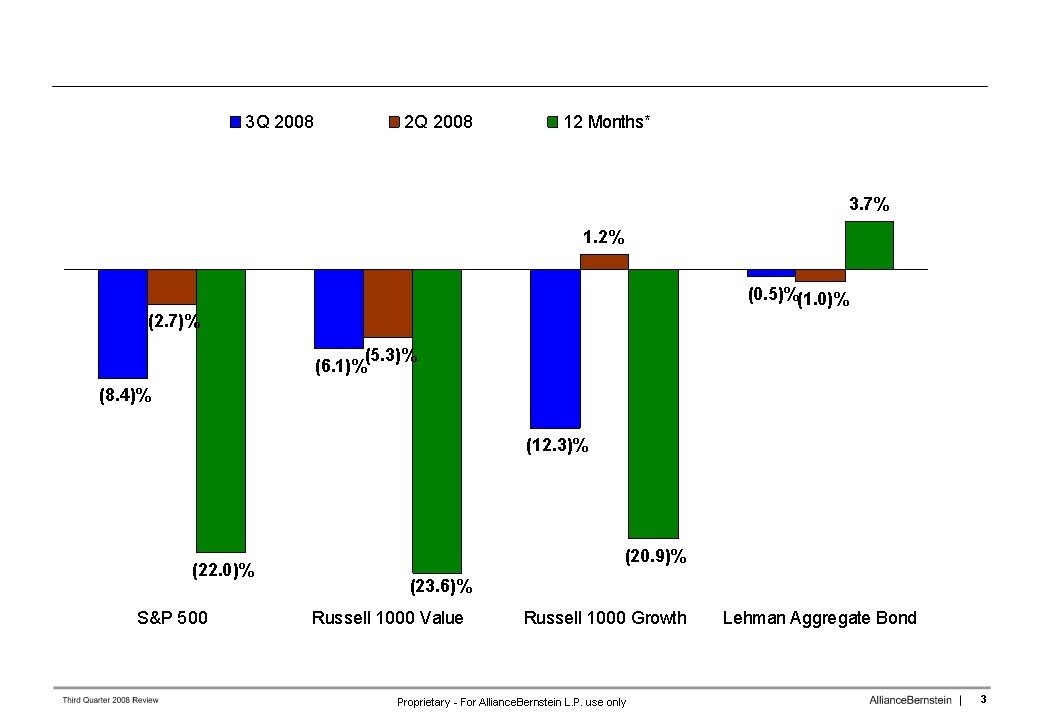

*12

months ending September 30, 2008.

Market

Performance - US

AllianceBernstein

4

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

5

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

6

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

NOTE:

Percentages are calculated using AUM rounded to the nearest

million.

AllianceBernstein

7

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

8

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

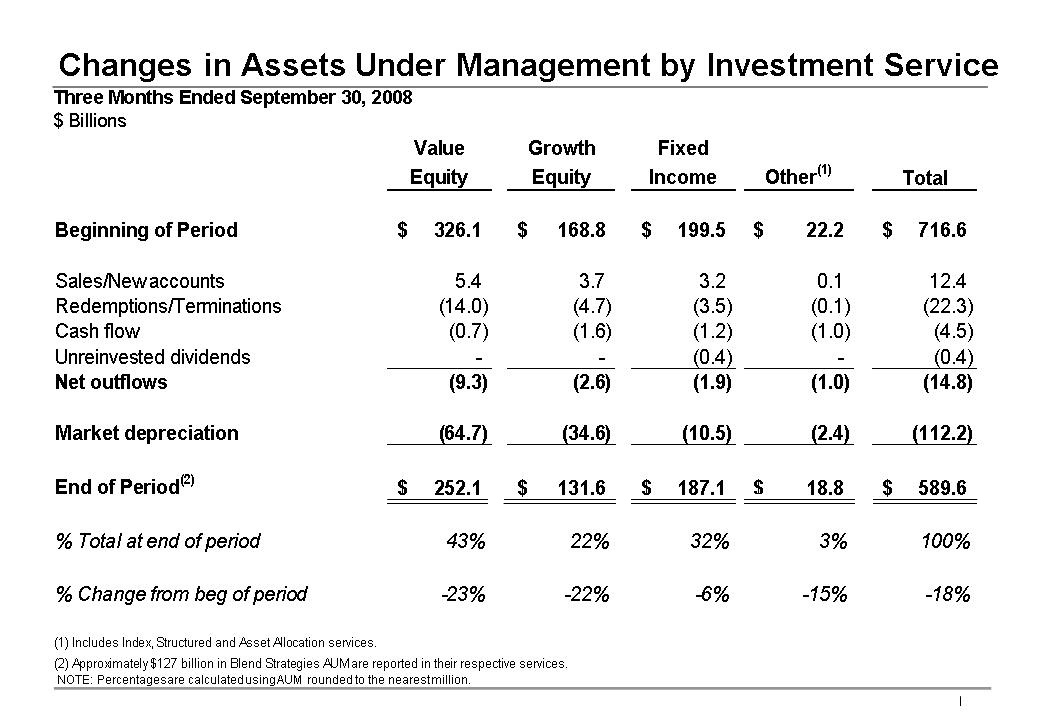

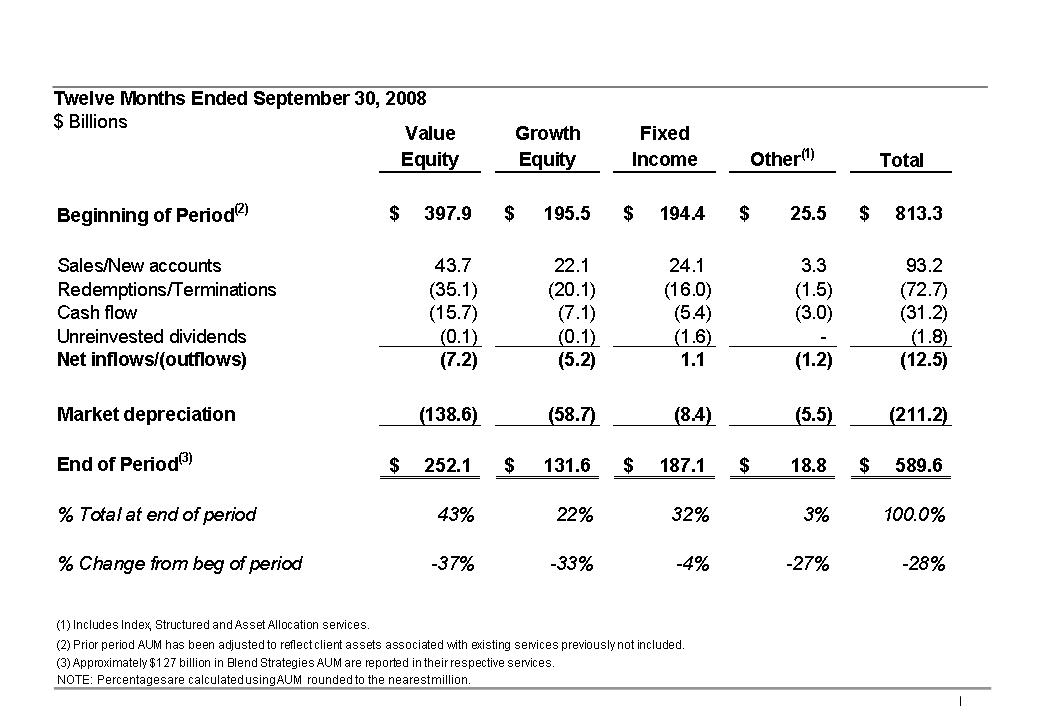

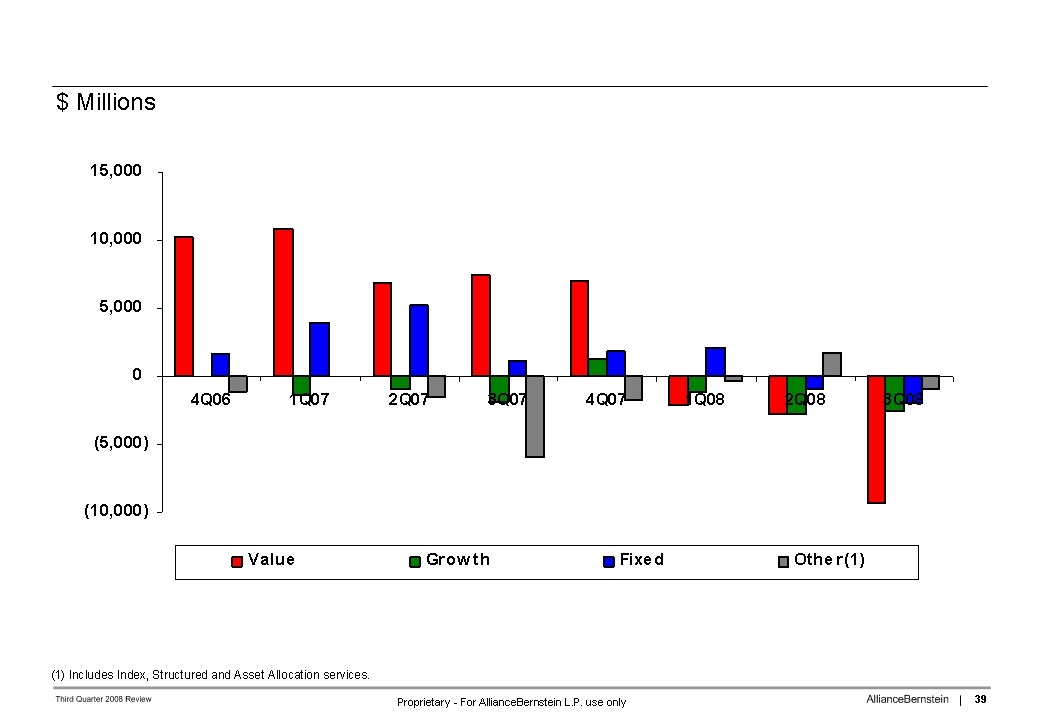

Changes

in Assets Under Management by Investment Service

AllianceBernstein

9

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

(1)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the

firm.

NOTE:

Percentages are calculated using AUM rounded to the nearest

million.

Institutional

Investments Highlights: 3Q08

AllianceBernstein

10

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

(1)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the

firm.

NOTE:

Percentages are calculated using AUM rounded to the nearest

million.

Retail

Highlights: 3Q08

AllianceBernstein

11

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

(1)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the

firm.

NOTE:

Percentages are calculated using AUM rounded to the nearest

million.

Private

Client Highlights: 3Q08

Alternative

Investment Services AUM*

*

Consists of Hedge Fund, Currency and Venture Capital

services

AllianceBernstein

13

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

14

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

Third Quarter 2008 Revenues

NOTE: Percentages

are calculated using revenues and expenses rounded to the nearest

thousand.

AllianceBernstein

15

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

Third Quarter 2008

Advisory Fees

NOTE: Percentages

are calculated using AUM rounded to the nearest million and revenues to the

nearest thousand.

AllianceBernstein

16

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

Third Quarter 2008

Operating Expenses

NOTE: Percentages

are calculated using revenues and expenses rounded to the nearest

thousand.

AllianceBernstein

17

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

NOTE:

Percentages are calculated using expenses rounded to the nearest

thousand.

AllianceBernstein

Third Quarter 2008 Compensation

& Benefits

AllianceBernstein

18

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

Third Quarter 2008 Net Income

(1)

"Operating Margin" = (Operating Income - Non-Controlling Interest in

Earnings)/Net Revenues

NOTE: Percentages

are calculated using revenues and expenses rounded to the nearest

thousand.

AllianceBernstein

19

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

(1)

Excludes insurance recoveries related to class action claims processing

error.

NOTE:

Percentages are calculated using income, earnings and expenses rounded to the

nearest thousand.

AllianceBernstein

Holding Financial Results

AllianceBernstein

Third

Quarter 2008 Review

Third

Quarter 2008 Review

Lewis

A. Sanders

Chairman & Chief Executive Officer

Chairman & Chief Executive Officer

Any

forecasts in this material may not be realized. Information or opinions should

not be construed as investment advice.

October

22, 2008

AllianceBernstein

23

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Market

Environment

AllianceBernstein

24

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

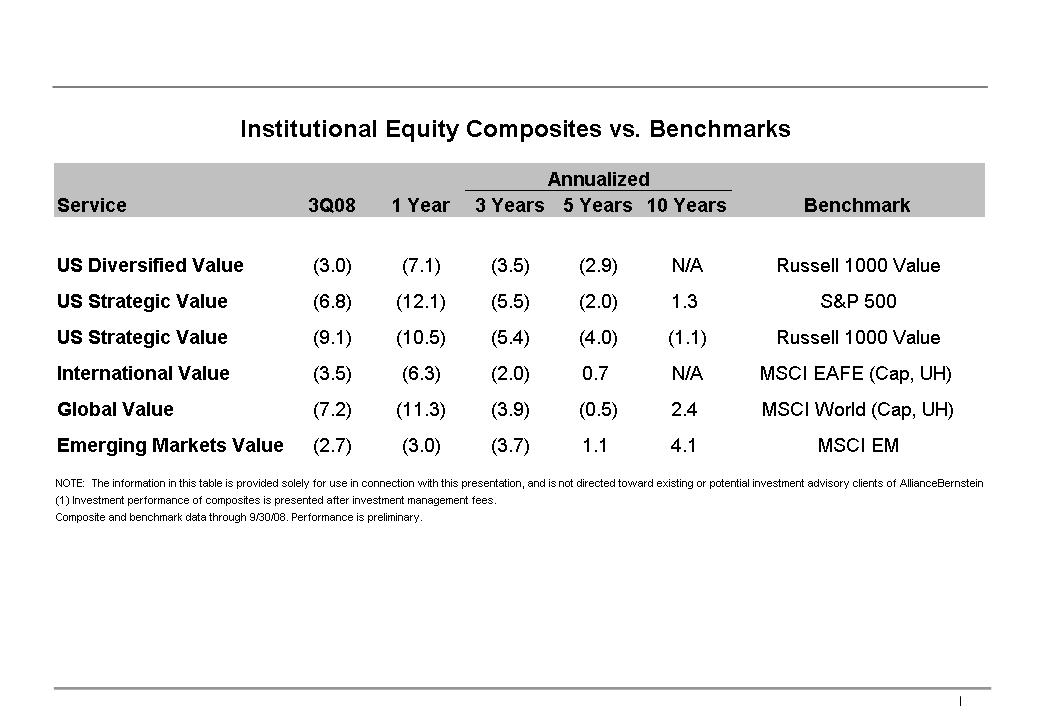

Relative

Performance: Institutional Growth Equity (After

Fees)(1)

AllianceBernstein

25

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Relative

Performance: Institutional Value Equity (After

Fees)(1)

AllianceBernstein

26

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

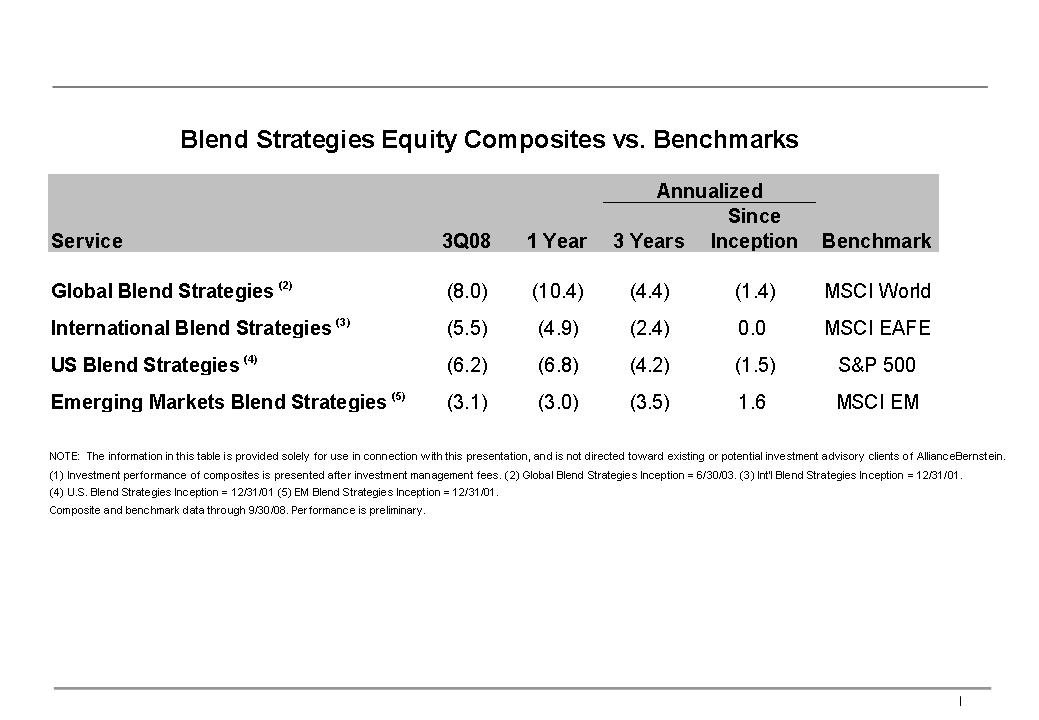

Relative

Performance: Blend Strategies (After

Fees)(1)

AllianceBernstein

27

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

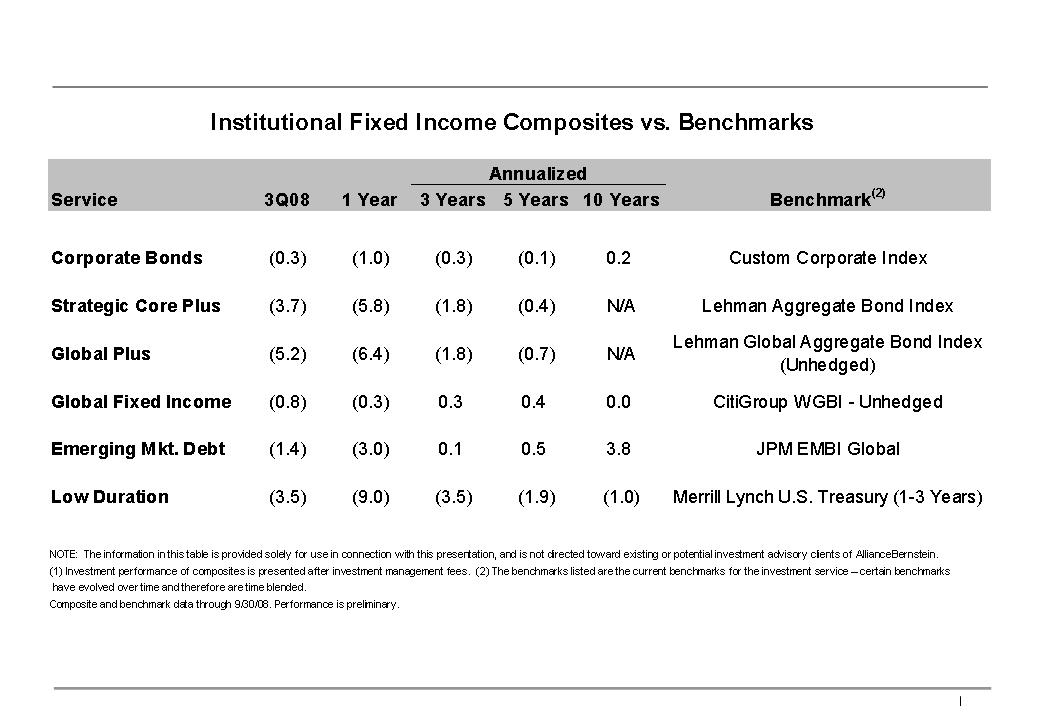

Relative

Performance: Institutional Fixed Income (After

Fees)(1)

AllianceBernstein

28

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

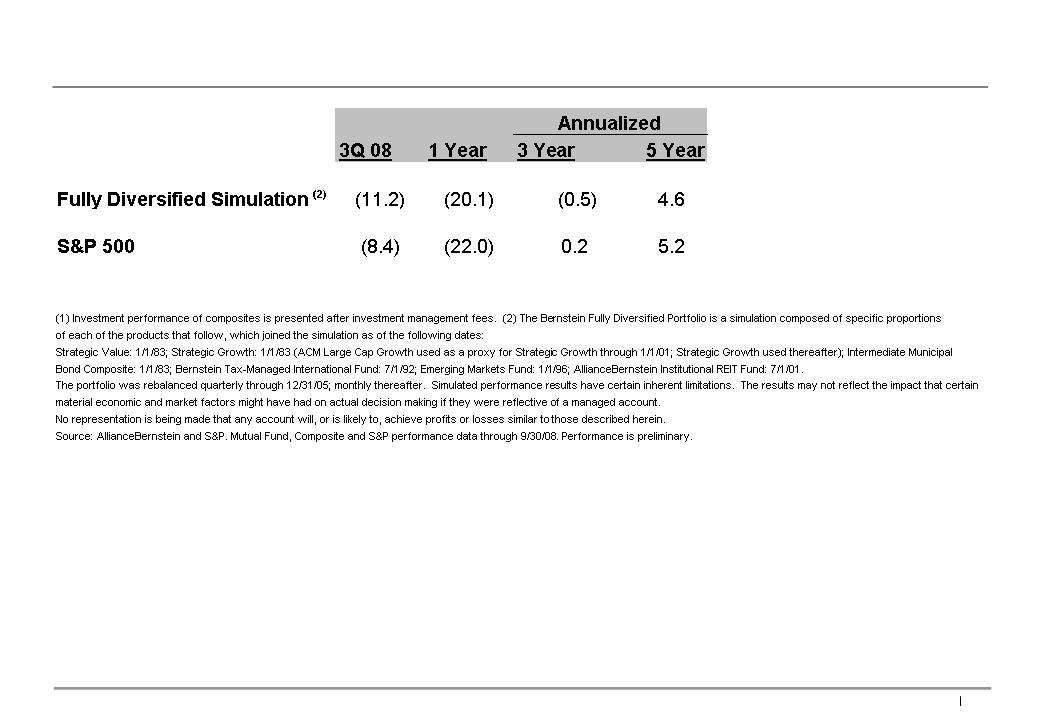

Absolute

Performance: Private

Client

(After

Fees)(1)

AllianceBernstein

29

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Relative

Performance: Retail Growth Equity (After

Fees)(1)

AllianceBernstein

30

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Relative

Performance: Retail Value Equity (After

Fees)(1)

AllianceBernstein

31

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Relative

Performance: Retail Fixed Income (After

Fees)(1)

AllianceBernstein

32

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

Relative

Performance: Wealth Strategies (After

Fees)(1)

AllianceBernstein

34

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

35

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

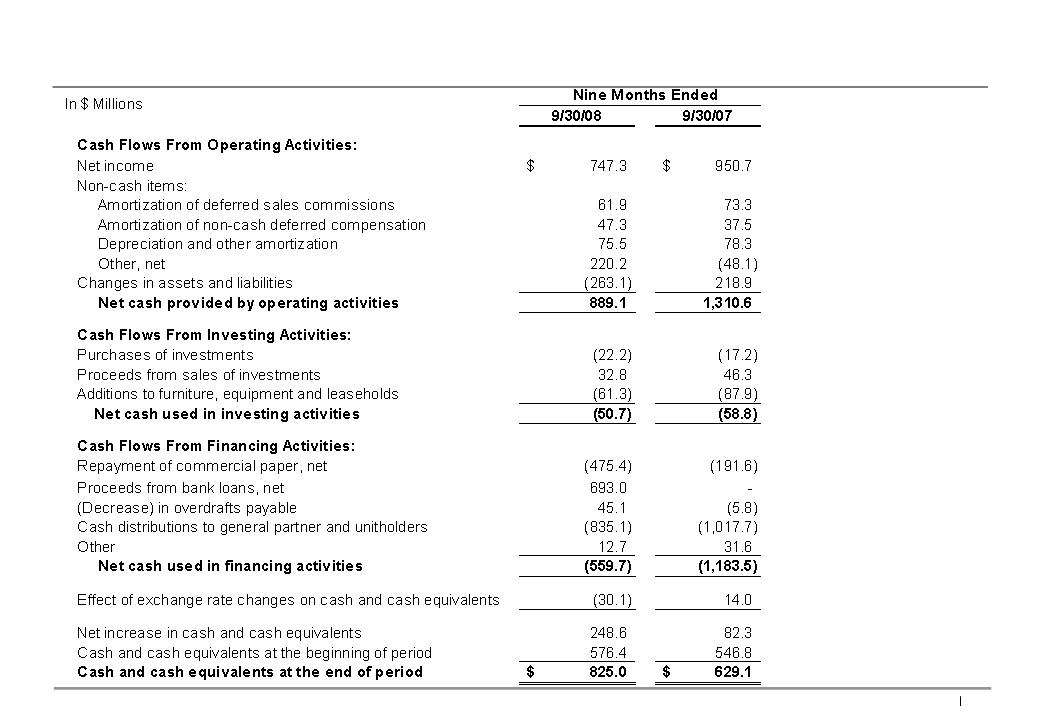

Consolidated Statement of Cash Flows

AllianceBernstein

36

Third

Quarter 2008 Review

Proprietary - For

AllianceBernstein L.P. use only

AllianceBernstein

Headcount

AllianceBernstein

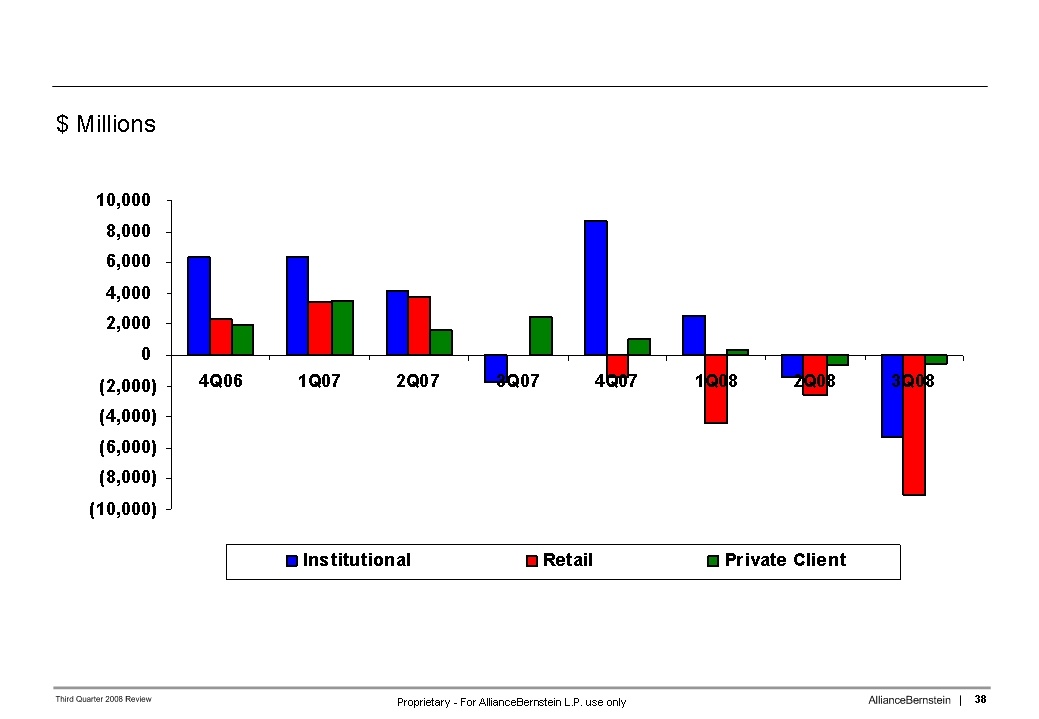

Total Net Flows

AllianceBernstein

Net Flows by Distribution Channel

AllianceBernstein®

and the AB AllianceBernstein Logo are trademarks and service marks owned by

AllianceBernstein L.P.

Exhibit

99.03

Event

ID: 1994062

Culture: en-US

Event

Name: Q3 2008 AllianceBernstein Holding L.P. Earnings Conference

Call

Event

Date: 2008-10-22T21:00:00 UTC

P:

Operator;

C: Philip

Talamo; AllianceBernstein Holding L.P.; Director, IR

C: Jerry

Lieberman; AllianceBernstein Holding L.P.; President and COO

C: Lew

Sanders; AllianceBernstein Holding L.P.; Chairman and CEO

P: Craig

Siegenthaler; CSFB; Analyst

C: Robert

Joseph; AllianceBernstein Holding L.P.; SVP and CFO

P: Marc

Irizarry; Goldman Sachs; Analyst

P:

Cynthia Mayer; Merrill Lynch; Analyst

P: Robert

Lee; Keefe, Bruyette & Woods; Analyst

P:

William Katz; Buckingham Research Group; Analyst

P:

Christopher Spahr; Deutsche Bank; Analyst

Operator: Thank you for

standing by, and welcome to the AllianceBernstein third quarter 2008 earnings

review. At this time, all participants are in a listen-only mode. As a reminder,

this conference is being recorded, and will be replayed for one week. I would

now like to turn the conference over to the host for this call, the Director of

Investor Relations for AllianceBernstein, Mr. Philip Talamo. Please go

ahead.

Philip Talamo: Thank you Sade.

Good afternoon, everyone, and welcome to our third quarter 2008 earnings review.

As a reminder, this conference call is being webcast, and is supported by a

slide presentation that can be found in the Investor Relations section of our

website at www.alliancebernstein.com/investorrelations.

Presenting our results today is our President and Chief Operating Officer, Jerry

Lieberman. Following Jerry's remarks, our Chairman and CEO, Lew Sanders, will

briefly address the audience. Our CFO Bob Joseph will also be available to

answer questions after our formal remarks.

I would

like to take this opportunity to note that some of the information we present

today is forward-looking in nature, and, as such, is subject to certain SEC

rules and regulations regarding disclosure. Our disclosure regarding

forward-looking statements can be found on page 2 of our presentation, as well

as in the Risk Factors section of our 2007 10-K. In light of the SEC's

Regulation FD, management is limited in responding to inquiries from investors

and analysts in a non-public forum. Therefore, we encourage you to ask all

questions of a material nature on this call. Now, I'll turn the call over to

Jerry.

Jerry Lieberman: Thank you,

Phil and good afternoon to everyone on the call. It's obvious to all that we're

going through terribly turbulent capital markets and that these conditions have

had a sharply negative impact on our absolute performance for our clients, and

indeed, on our financial results for our unitholders. For the second quarter in

a row, assets under management, revenues, net income and distributions, as well

as expenses, are all down versus the corresponding quarter of 2007, trends that

must be and are being addressed.

Additionally,

our relative performances suffered significantly, impacted by our exposure to

sectors and individual stock selection most adversely affected by the global

financial crisis, as well as our significant non-U.S. exposure during a period

of a strengthening U.S. dollar.

As far as

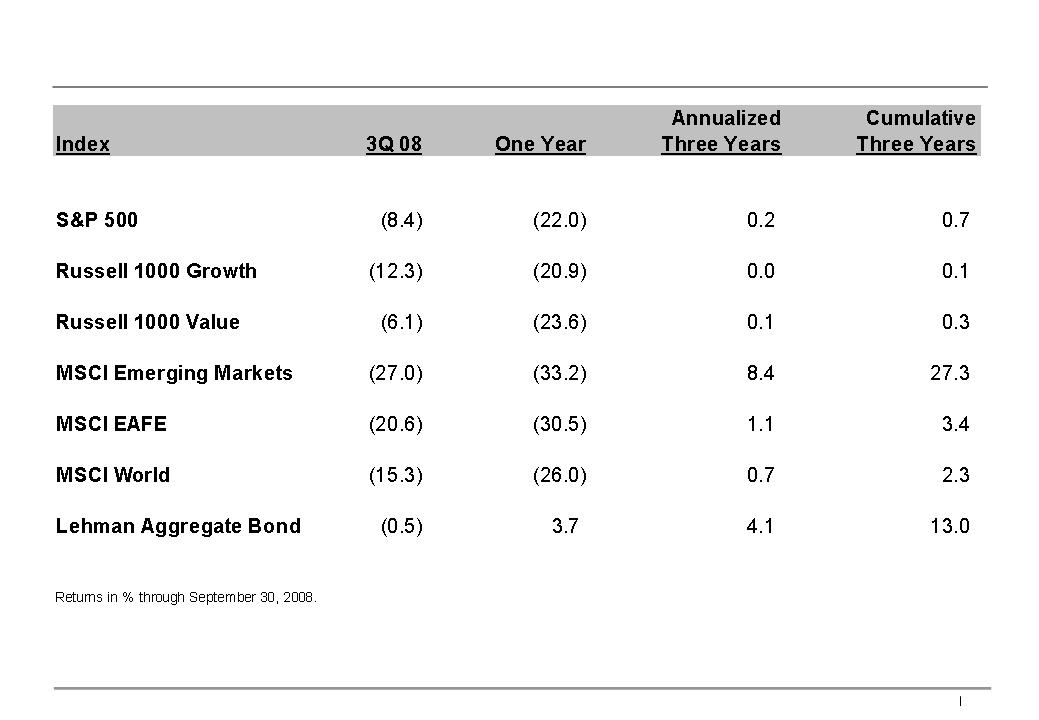

the capital markets are concerned, U.S. equity indices, shown on Display 3, were

down 8.4% to 12.3% for the quarter, and 20.9% to 23.6% for the 12 months ended

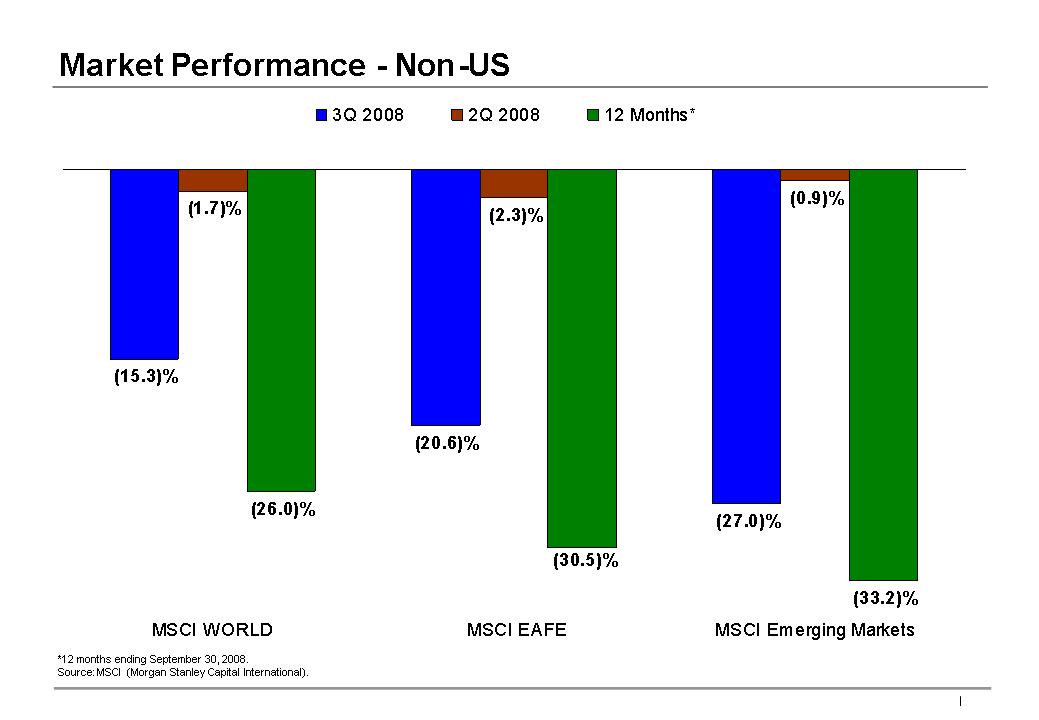

September. Non-U.S market indices, shown on Display 4, declined dramatically

from 15.3% to 27% for the quarter, and from 26% to over 33% over the last 12

months.

Displays

5-8 reflect our assets under management roll-forwards by channel and by major

asset class for both the quarter and the trailing 12 months. These displays show

that our assets have declined by $127 billion and $224 billion for the quarter

and trailing 12 months, respectively, overwhelmingly due to the market

depreciation in both Value and Growth equities.

Now,

let's turn to Display 9, where I'll begin my discussion on channel highlights.

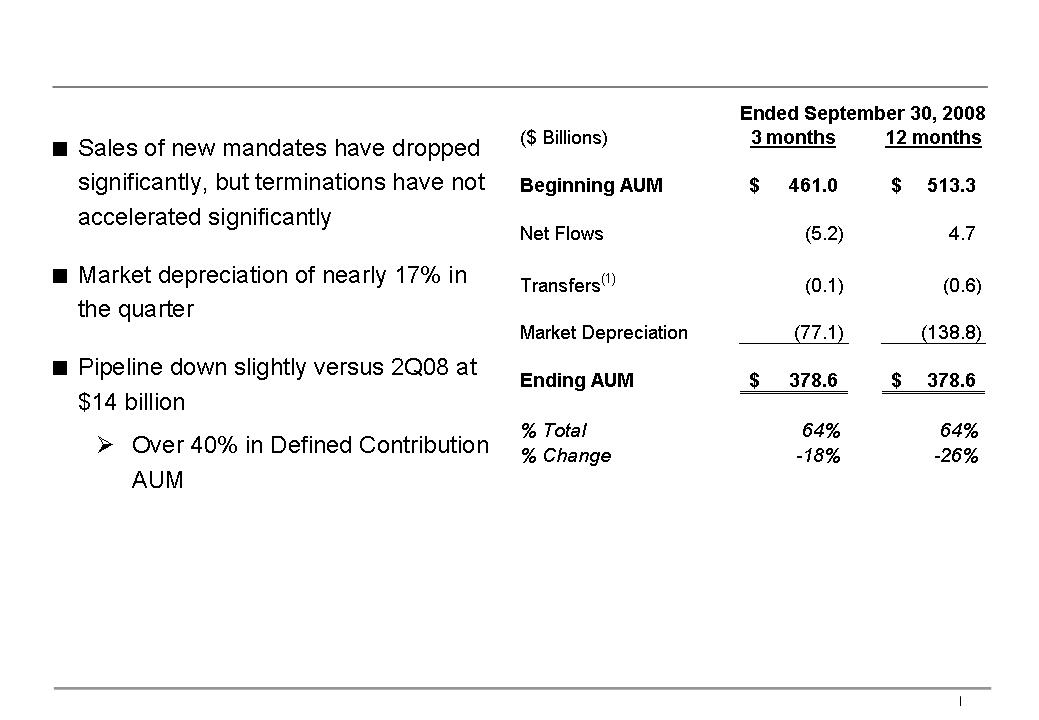

In our Institutional Investment distribution channel, AUM declined by 18% in the

quarter, almost entirely due to market depreciation. It is important to note

that although our net outflows accelerated versus the previous quarter to $5.2

billion, these outflows are more a function of fewer new mandates, rather than a

significant loss of client accounts or cash flow withdrawals. Aside from the

defined contribution plan mandate wins, we are seeing institutional investors

put new mandates on hold while the market turmoil plays itself out. Accordingly,

our pipeline of won but unfunded Institutional mandates declined slightly to $14

billion, with over 40% in defined contribution AUM, a key strategic initiative

for our firm.

On

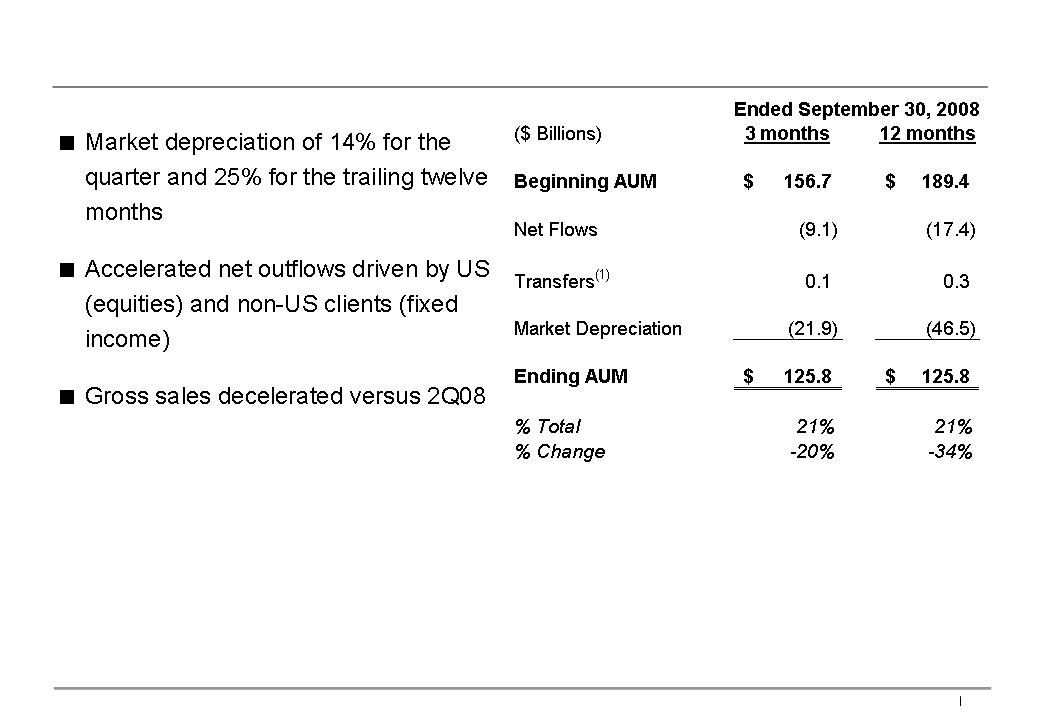

Display 10, you can see that our Retail channel assets decreased by 20% for the

quarter, due primarily to market depreciation of 14%. However, net outflows in

this channel were substantial as sales have virtually collapsed and redemptions

have indeed increased. This is a phenomenon that began in Asia but has now

spread to the U.S. Net outflows accounted for over 29% of the decline, and were

most notable in equity services for U.S. clients and fixed income services for

non-U.S. clients.

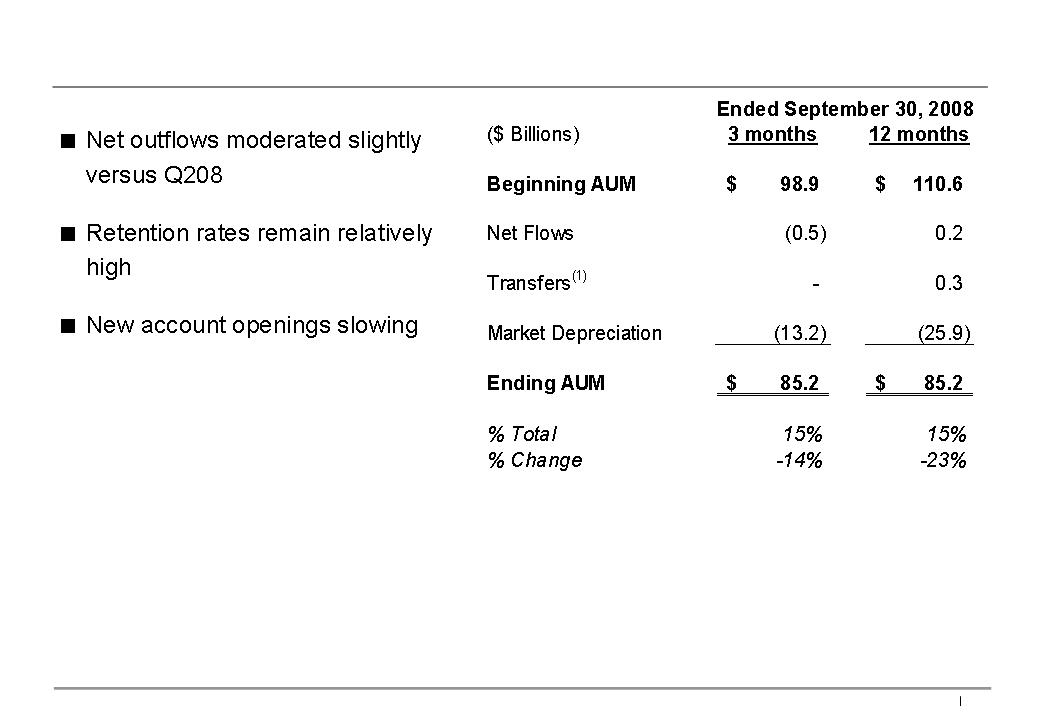

Turning

to Display 11, you'll see that our Private Client channel AUM fell by 14% during

the quarter, a smaller decline than our other channels, incurring modest net

outflows at a rate actually slightly lower than the second quarter of 2008. Even

more so than in our Institutional Investment channel, let alone our Retail

channel, our Private Client group's assets are our stickiest, that is, our most

persistent. We attribute Private Client loyalty to constant high quality client

servicing and the penetration of our asset allocation services that have served

our clients well in these tumultuous times. However, we have seen a slowing of

new account openings.

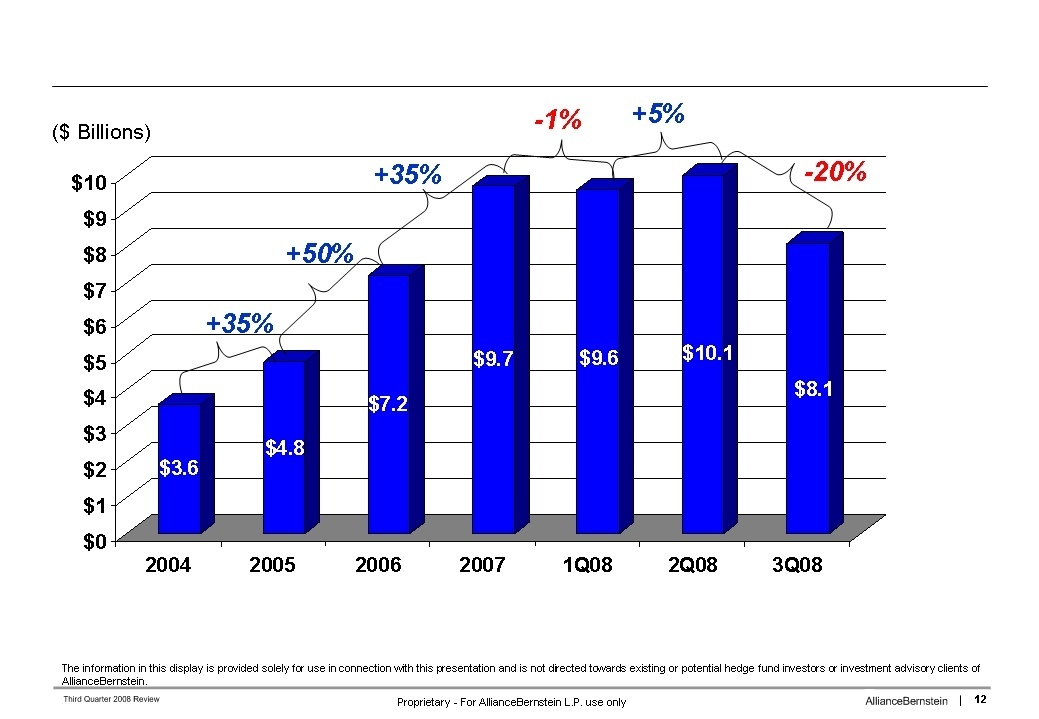

Display

12 shows that during the third quarter of 2008, the total AUM associated with

our suite of Alternative Investment Services fell by 20% sequentially to $8.1

billion. This decline in assets was predominantly due to market depreciation in

Hedge Fund services.

On a more

positive note, as cited on Display 13, Institutional Research Services

established a new record for quarterly revenue at $125 million, with increased

market volumes and increased market share each contributing to these robust

results. The 21% in year-over-year growth was mostly driven by our U.S.

operations. Also, our sell-side analysts posted excellent results in

Institutional Investor’s just released All-America poll- in fact, the best ever

for our firm. The firm as a whole placed in the top 10 for the fifth consecutive

year at number 6 and every single analyst that began 2008 as a publishing

analyst was recognized in the survey, with 85% in the top 3 in their sector,

including 10 “number ones”.

Moving to

the income statement, I'll begin with the discussion of revenues as shown on

Display 14.

Net

revenues fell by 27% to $841 million, the first time in two years that quarterly

net revenues were below $1 billion. Over 50% of the $312 million year-over-year

revenue decline was due to an 18% decrease in Advisory Fees, as AUM fell

substantially in all three buy-side distribution channels.

About 46%

of the decline in Net Revenues was due to a $142 million swing in Investment

Gains and Losses, principally the result of mark-to-market losses on investments

related to deferred compensation of $123 million, compared to $2 million in

gains for the third quarter of 2007. As a reminder, these mark-to-market gains

and losses have a corresponding offset in current and future incentive

compensation expense.

The sharp

percentage decline in Distribution revenues was due to lower Retail AUM. Largely

offsetting this decline was the strong increase in Institutional Research

Services revenue that I noted earlier. The substantial percentage decrease in

Dividend and Interest income, as well as the offsetting decrease in Interest

Expense below, reflect the late 2007 outsourcing of our prime brokerage

services, as well as lower interest rates.

Display

15 provides additional analysis of Advisory Fees. Lower base fees represent

almost 90% of the $157 million decline in Advisory Fees, with the lack of

performance fees making up the remainder. You will note that the decrease in

base fees was 1,200 basis points lower than the decrease in period-ending AUM,

yet equal to the decrease in average AUM. This was due to the fact

that much of the third-quarter's market depreciation occurred in September, so

the impact on average AUM for the quarter was less severe than the impact on

period-ending AUM.

All three

buy-side distribution channels incurred a double-digit decline in revenue, with

Retail and Institutional Investments down around 20%, and our Private Client

channel down about 13%, which were in line with their respective decreases in

AUM.

Operating

expenses, as shown on Display 16, declined by $181 million, or 24%,

year-over-year. About two-thirds of the decrease came from employee compensation

and benefits, which fell by $118 million, or 26%, and will be discussed in

greater detail on the next display.

Promotion

and Servicing expense decreased by 19%, or $31 million, in the quarter. Lower

distribution plan payments accounted for approximately one- half of this decline

and controllable expenses such as travel, printing and mailing expenses

accounted for approximately one-third, with the balance due to lower

amortization of deferred sales commissions.

General

and Administrative expenses were down 19% as a $35 million insurance recovery

related to the fourth quarter 2006 charge for a class action claims processing

error was partially offset by higher data processing costs resulting from

increased trading volumes and foreign exchange losses versus gains in the

prior-year quarter.

Display

17 details Employee Compensation and Benefits which fell 26% versus the third

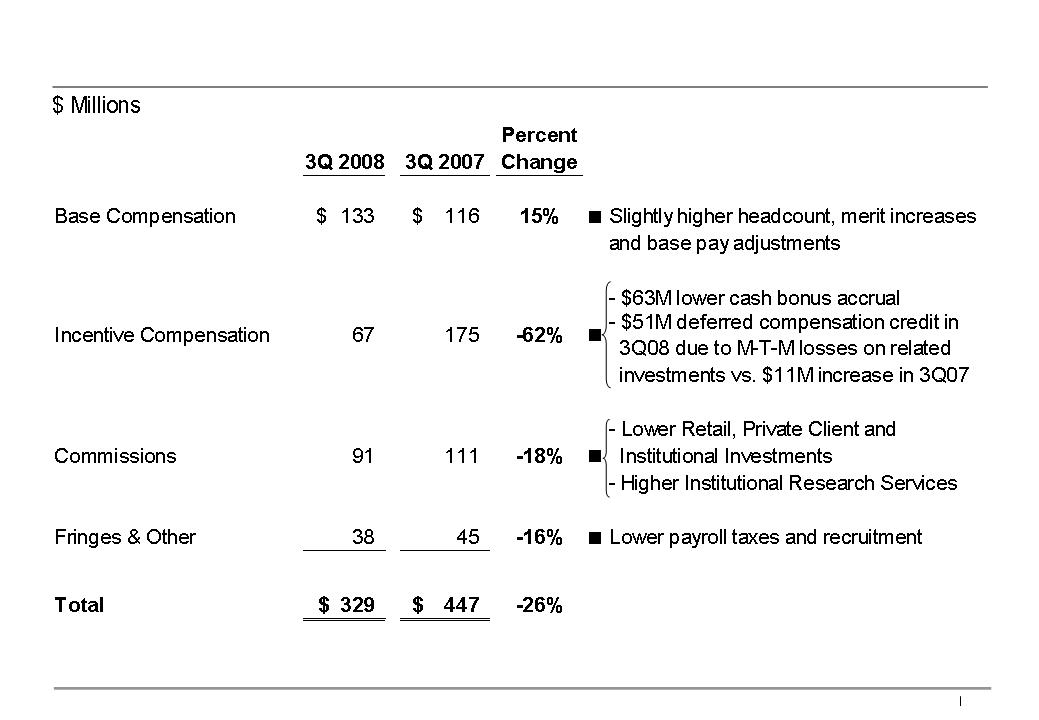

quarter of 2007 to $329 million. Base compensation was up 15% versus last year,

due to slightly higher headcount, merit increases and base compensation

adjustments. Headcount increased versus the second quarter of 2008 by only 25

employees, to 5,660, a topic that Lew will address in more depth later on in

this call.

Third

quarter Incentive Compensation expense was down 62% year-over-year, due to $63

million in lower accruals for cash bonuses in addition to mark-to-market losses

on investments related to employee deferred compensation. The mark-to-market

losses decreased incentive compensation by $51 million, versus an $11 million

increase in the third quarter of 2007. Investments related to employee deferred

compensation stood at $519 million at the end of the third quarter of '08, down

almost 20% sequentially.

Commissions

fell by 18%, as declines in our three asset management channels were partially

offset by an increase in Institutional Research Services. Fringes and other

expenses fell by 16%, predominantly due to lower payroll taxes, a function of

lower year-end bonus accruals, as well as lower recruitment

expenses.

On

Display 18, you will find a summarized income statement for the Operating

Partnership. Despite aggressive management of controllable expenses, the severe

decline in AUM, and consequently revenues, led to a 37% drop in Net Income and a

410 basis point decline in operating margin.

Display

19 details the impact on the Holding company. Here you will note that while Net

Income for the Holding Company fell 39% and is in-line with the decline for the

Operating Partnership, our distribution per Unit actually fell by 50%. This was

due to excluding a $35 million insurance recovery from distributions in the

quarter. You will recall that when we took a $56 million charge against earnings

in the fourth quarter of 2006 for a class action claims processing error, we did

not reduce the distribution for that quarter and fourth quarter '06 distribution

was $0.21 greater than EPU. This $35 million was a part of the resolution of our

insurance and claims, a portion of which we are still hopeful will be realized

in the future.

Before I

wrap up, I would like to briefly address the overall health of

AllianceBernstein. Our firm is one of the world’s largest organizations focused

exclusively on investment research and management for our clients. We are not a

commercial bank, and we neither originate mortgages nor hold proprietary

positions in mortgage-backed securities that are at the epicenter of the recent

credit problems. Nor are we an investment bank or an insurance company that

engages in investment banking activities, thereby having direct exposure to

troubled assets. Additionally, AllianceBernstein has long maintained a

conservative balance sheet, which is reflected in our strong long-term credit

ratings, with S&P at AA-, Moody's at A1, and Fitch at A+.

Clearly,

as securities valuations globally have dropped, so have our assets under

management and, accordingly, our profitability. However, in the face of a likely

continuation of capital markets turmoil, Lew and I are confident in our

investment and client service professionals, and we are confident that they will

work closely with our clients to see them through this period of stress and

volatility and that our management team will continue to control expenses. Our

balance sheet is strong, our intellectual capital is intact, our expenses and

capital outlays are being aggressively managed while we continue to invest in

our most important strategic initiatives. Therefore, we firmly believe

AllianceBernstein is well-positioned for the future and that our efforts will

benefit all of our stakeholders in the long run. And now, I will turn the call

over to Lew.

Lew Sanders: Thanks,

Jerry.

As Jerry

has highlighted, extremely adverse capital markets conditions are placing

serious pressure on the firm. While we don't face the capital adequacy issues or

the funding problems that have become problematic for some in the industry, we

do face challenges of a different kind.

The

collapse in the equity markets throughout the world, coupled with weak relative

returns, has resulted in a dramatic decline in assets under management. The

strength of the U.S. dollar has exacerbated this effect, given the global

character of our product array. In addition, as Jerry outlined in his remarks,

widespread client anxiety has curtailed the flow of new business and increased

redemptions, especially among retail investors.

With

assets under management being the key driver of our revenue, there is now a

clear need to align the cost structure of the firm with a meaningfully lower

revenue run rate. In the past, we have been reluctant to react to short run

fluctuations in revenue - but these are not normal times.

As you

all know, a substantial portion of our operating expense structure is variable

in nature and that will be helpful in reducing costs. For example, Incentive

Compensation, both cash and deferred, will fall sharply, especially in the upper

ranks of the firm. But we have to do more. We have to right-size the Company to

reflect its reduced asset base.

Now, as

we proceed down this path, we will be mindful, however, of three equally

important objectives: First and foremost, that we don't do anything

that could in any way interfere with our ability to deliver on the

firm's mission -- the long-term investment success of our clients and their

piece of mind, a formidable task, to say the least, given the current market

turmoil, but to which we are steadfastly dedicated.

Second,

we need to ensure that despite the current pressures we position the firm to

grow when the turmoil subsides. Thus, we must continue to fund those initiatives

that we see as critical to our long term growth -- and let me assure you that

that's our plan.

And

third, we have to remain a meritocracy. Now, that's a worthy objective at all

times, but it is even more important in difficult times.

Consistent

with these objectives, we will not be pursuing formulated headcount reductions.

Rather, we've asked the leadership of each business unit to consider carefully

and thoughtfully the number of employees they need to manage their areas, given

our reduced scale. And of course, those numbers are going to be lower than we

now have.

This

process will be implemented, in large part, in this year's fourth quarter, and

will require a charge against earnings. The size of that charge has not yet been

determined, but the payback in reduced costs will far more than offset it in

2009.

Now,

letting people go we have respect and affection for is really hard, perhaps the

hardest thing to do in business -- but we simply have no choice. Fortunately, we

believe we have the depth and breadth of talent to do so without damaging the

firm's future.

Now, if

there's one benefit of age -- and frankly, it's the only one I can think of – it

is that you have seen tough times before. And I have. I lived through many bear

markets when I first entered the business in 1966, and then in 1970, 1982 and

1987, bear markets which produced price declines of 15 to 30%. I lived through a

devastating bear market in 1973 and 1974, where the cumulative decline reached

43%. And of course, more recently, the bursting of the internet bubble, which

before it came to a close in late 2002 produced a decline of 45%.

Let me

assure you that all of these episodes felt just as terrible as this one does. At

the trough they felt as if there was no hope, that the problems that created all

the trouble were intractable, and would take years to resolve. But in all of

those cases, countervailing forces surfaced, some as a function of government

actions, others from market-based adjustments, and the tide turned. Investment

performance was restored and growth resumed.

I remain

highly confident that the actions we are taking will position us to take

advantage of that recovery for our clients and for the firm. And if history is a

guide, it will arrive sooner and be stronger than generally

expected.

And now,

for your questions.

Operator: Management has

requested that you please limit your initial questions to two in order to

provide all callers an opportunity to ask questions. We welcome you to return to

the queue to ask follow-pp questions. It is AllianceBernstein’s practice to take

all questions in the order in which they are received and to empty the queue

before ending the call. Your first question comes from William

Katz.

William Katz: Thank you, and

good afternoon. My first question is probably on everyone's mind. I am trying to

think about quantifying the potential cost reductions in light of the decline in

revenues. How should we think about that? And when looking at your earnings over

the last several years, and your assets are now back to where they were in the

first quarter of '06 in round numbers, your compensation is relatively flat. So

I am struggling to see where the expense savings would come from.

Jerry Lieberman: Bill, as Lew

mentioned, we're still putting together a plan, but one that we will be

executing through the fourth quarter. This will be a reduction in force that's

unprecedented in the 40-year history of our firm. This is going to be

meaningful. We're talking about severance in the tens of millions of dollars,

all of which we hope to have a payback on, and expect to have a payback on, in

'09.

William Katz: Okay. The second

question I have is around the hedge fund and alternatives businesses. If I look

back at that slide, I think it was down about 20% sequentially. Is it fair to

assume that the bulk of that decline is performance-related?

Jerry Lieberman: It's all

performance-related. Our hedge funds give our clients twice a year opportunities

to get out of the hedge funds and the next period coming up will be the end of

the year. It's still early for those decisions to be made but I can tell you

that as of now, it hasn't shown to be meaningful. But they have a month to

really make the decision, Bill. But everything you see here is

performance-related.

William Katz: Just so I

understand it, any redemption of that would then be in the January

quarter?

Jerry Lieberman: That's

right.

William Katz: Could you give

us an update on the percentage of hedge funds that have high water marks, and

how much of those are now greater than 10%, consistent with your 10-Q

disclosure?

Jerry Lieberman: Bill, I don't

have that with me.

Lew Sanders: Bill, I think you

can assume that the high water marks are a meaningful impediment to the

re-emergence of performance fees for the foreseeable future

William Katz: Okay. Thank you,

Lew.

Operator: Your next question

comes from Craig Siegenthaler.

Craig Siegenthaler: Thanks.

Can I get some clarification on the general and administration expenses? You had

about $36 million of insurance recoveries benefiting that line but on top of

that, you said there was some other kind of one-time negatives against that. How

should we think about the true run rate for that item?

Jerry Lieberman: I'm not sure

the others were one-time negatives.

Craig Siegenthaler: The data

processing costs --

Jerry Lieberman: Those aren't

one-time at all. Those are data processing costs that are related to

transactions in the trading business. So, to the extent that the volume of

trading increases in the business, those are going to go up, if trading

decreases, those will go down. Those are volume-related expenses. You can look

at foreign exchange as one-time, and it depends on how the dollar strengthens or

weakens from quarter to quarter.

Lew Sanders: So the bottom

line here is if you add back the insurance adjustment that represents a

reasonably good estimate of the run rate. And of course, we'll be working hard

to do what we can to contain those costs in the period ahead, but there is a

substantial fraction of those costs that are fixed.

Craig Siegenthaler: Got it.

And then on net flows. When I think about your institutional business, a lot of

the growth came from outside the U.S. with large institutions over the last one

to two years. Those clients are newer, and when looking at terminations in that

business, they are holding in pretty well in institutions. In previous cycles

when you had relative performance and absolute performance being very low, where

did terminations relative to the AUM kind of flow here?

Jerry Lieberman: To date, as I

mentioned in the call, except for our mutual funds, the clients have been

staying with us, and pretty steadily to date. And obviously they're looking at

both absolute and relative performance. They're looking at how we are servicing

them and so far, they have been holding on pretty strongly. Does that answer

your question, Craig?

Craig Siegenthaler: Yes. Thank

you.

Operator: Your next question

comes from Marc Irizarry.

Marc Irizarry: Great. Lew,

maybe you can take this one. If you just think about returns over time, active

versus passive, do you expect, given where the three and five year numbers are

relative to the benchmark now, that institutions may take another look at their

allocation between passive and active managers? And then I have a follow-up.

Thanks.

Lew Sanders: They may well,

Marc, but if history is a guide in this subsequent recovery which, once again,

based on history, will be sooner and stronger than might appear likely, active

returns tend to actually be quite strong. So looking right now, with end point

sensitivity focused on an extremely adverse moment in time, it might appear as

if there's quite a lot of vulnerability, but that could well change in a

subsequent recovery and moot the issue about allocation between passive and

active that you are suggesting might apply.

Marc Irizarry: And then,

Jerry, one for you. Can you give us a sense of what sort of a run rate of

revenue is going to be heading out? And clearly, you don't want to cut into

muscle, but what's the target operating margin? How should we think about the

target operating margin for this business on a longer term basis?

Jerry Lieberman: Marc, we've

never had margin targets in either the good times or the bad times, and we don't

have one now. There's a lot of leverage in this business, so it's hard to

forecast. What I can assure you and assure the unit holders is if we continue to

see the turmoil that we've seen, and if we see markets continue to go down and

our revenues go down, we will address this in an appropriate

manner.

Marc Irizarry: Great, I'll get

back in the queue.

Operator: Your next question

comes from Cynthia Mayer

Cynthia Mayer: Hi, good

afternoon. Circling back to the cost-cutting, if you are not thinking about it

in terms of operating margin, I'm wondering what will you be using to gauge how

much is enough AUM decline or revenues decline? How will you know when the

business has come back to you with their numbers, whether that looks good enough

for you?

Jerry Lieberman: What we do

here is look at revenues, not AUM and again, we've never had margin targets, and

we've never had AUM targets, but we are consistently, and very, very frequently

reforecasting our revenues, even daily, because of the systems that we have in

place. We are looking for what is going to happen to our P&L going forward,

and do we have the right structure against what that P&L is. Now clearly,

what we've built up in the last few years is a structure to be a larger firm,

and we had $817 billion a year ago, and we built ourselves up to accommodate

client needs for a firm that size. We are taking on here a downsizing which is

unprecedented in the history of either Alliance or Bernstein in a serious

way.

Lew Sanders: And Cynthia, let

me just add that the objective here is to ensure we successfully negotiate

through what is already a deep trough. That's the objective, not only by the way

we form portfolios for clients, but by the way we manage the firm. So when we

are thinking about cost structure targets, it's with that in

mind.

Cynthia Mayer: Okay. I was

just looking back at what happened in 2001. It looked like you cut operating

expenses by 11%. Are you using that at all as an example of how you should cut

costs at this time?

Lew Sanders: It is

already obvious that we are well above the contraction and expense that was

necessary then and we are, as we've described, embarking on a substantial

additional reduction in expense in the period ahead.

Cynthia Mayer: Okay, great.

And just a very quick mechanics question. The charge against earnings in fourth

quarter, would that lower the cash distribution or not affect it?

Jerry Lieberman: Yes, it will,

Cynthia. That's a cash charge that will affect the distribution. Although as

we've said, we're looking at a quite a quick payback in '09.

Cynthia Mayer: Great. Thank

you.

Jerry Lieberman: Let me just

say this, and this is both for Cynthia and Marc and probably for Bill who has

been asking this question about G&A since I joined the firm. When you look

at G&A, between technology related, a lot of which is infrastructure, and a

significant part is in deep variable costs, it’s office-related and is about

$120 million for the quarter. So, a lot of these costs are indeed fixed, unless

there's a turn in the business, because there's buying related expenses in

there. And then in the past, we've done a pretty good job at rationalizing

space, but you can do that only if indeed space frees up in the

firm.

Operator: Your next question

comes from Robert Lee.

Robert Lee: Thanks, good

afternoon. Lew, maybe you could highlight for us some of the continuing ongoing

areas for investment. Obviously, I'm assuming the DC business will be one clear

example, but could you maybe point out a couple of others?

Lew Sanders: Yes. Well, by far

and away, DC is the most important and although the thrust of this call is about

all of the pressure that the firm is now under because of capital market

conditions, we are actually very hopeful about our prospects in the DC market,

and have continued to do well in the competitions that we've entered, both in

medium, and especially in very large plans. We really think we have a compelling

value proposition, and that opportunity is really, really large. As I've

described, it's by far and away the largest institutional opportunity that's

available to us anywhere in the world. So it is perhaps the prime example of an

initiative that we will fully fund during this period of pressure. Others that

come to mind have to do with initiatives around new product development, which

holds promise for innovative services downstream. They are not all that

expensive to fund, but potentially meaningful contributors to the firm's revenue

and profitability, and perhaps more importantly, to the base of its intellectual

capital, as it might assist in managing some of the mainstream services. So the

R&D efforts are there too and will continue unaffected by these staff

cuts.

Robert Lee: Okay. And maybe

just one follow-up question. I mean, I know that so far, your institutional

client base has been sticky, and you haven't really seen too much in the way of

heightened redemptions there. But could you maybe talk about how you view your

consultant relationships in light of some of the performance challenges of the

past year or so that you've had? Are you finding that some of them have put you

in the penalty box and that may somehow impact your ability to accelerate growth

once the turn comes or anything like that?

Lew Sanders: That may come. It

hasn't as yet. As I think all of you know, investment performance is not about

trailing 12 months, or for that, matter trailing two years, it's about much

longer term records. And in some of the services where we have put up in the

last 12 months relatively weak returns, we have extremely competitive long-term

returns. This is not lost on a consulting community who know us well for a

really long time, and know us thoroughly, and understand our decision-making

processes, and actually can find in our history other such periods of adverse

return -- actually, in intervals that look something like the character of the

capital markets in the last 12 months. And so I think that a thoughtful review

of our results will show them to be actually well within the character of a

long-term performer, which is a really good one -- notwithstanding the last 12

months. So we're confident, pretty confident, that once recovery commences --

certainly once it has a degree of maturity -- that our competitive profile will

serve us relatively well -- on the assumption, of course, that in that recovery,

we perform as we anticipate. And of course, time will tell as to whether we

achieve those objectives.

Robert Lee: Okay. Thank

you.

Operator: Your next question

comes from William Katz.

William Katz:.I just want to

pick up on that last question. I'm curious, as you look at both the

institutional channel and also the private client channel, maybe to a lesser

extent retail, which is a bit more new in terms of its focus, you've always sort

of dubbed yourselves as risk adjusted return models. And yet, when I look at