UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the Securities Exchange Act of

1934

|

Date

of Report (Date of earliest event reported):

|

January

24, 2007

|

|

ALLIANCEBERNSTEIN

HOLDING

L.P.

|

|

(Exact

name of registrant as specified in its

charter)

|

|

Delaware

|

001-09818

|

13-3434400

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(Commission

File Number)

|

(I.R.S.

Employer Identification Number)

|

|

1345

Avenue of the Americas, New York, New York

|

10105

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

Registrant’s

telephone number, including area code:

|

212-969-1000

|

Check

the appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligations of the registrant under any of the following

provisions:

|

o

|

Written

communications pursuant to Rule 425 under the Securities Act (17

CFR

230.425)

|

|

o

|

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR

240.14a-12)

|

|

o

|

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17

CFR

240.14d-2(b))

|

|

o

|

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17

CFR

240.13e-4(c))

|

|

Section

2.

|

Financial

Information

|

|

Item

2.02.

|

Results

of Operations and Financial

Condition.

|

AllianceBernstein

Holding L.P. (“AllianceBernstein Holding”) is furnishing the news release it

issued on January 24, 2007 concerning financial and operating results for the

quarter and full year ended December 31, 2006 (“4Q06 Earnings Release”). The

4Q06 Earnings Release is attached hereto as Exhibit 99.01.

AllianceBernstein

Holding is furnishing its Fourth Quarter 2006 Review, dated January 24, 2007

(“4Q06 Review”). The Fixed Income performance figures displayed on slide 36

reflect corrections to the version originally presented. The 4Q06 Review

is attached hereto as Exhibit 99.02.

AllianceBernstein

Holding is furnishing a transcript of its conference call with analysts relating

to financial and operating results for the quarter and full year ended December

31, 2006 (“4Q06 Transcript”). The call took place on January 24, 2007. The 4Q06

Transcript is attached hereto as Exhibit 99.03.

The

4Q06

Earnings Release, 4Q06 Review, and the conference call with analysts (reflected

in the 4Q06 Transcript) include forward looking statements predicting increases

in net asset inflows, describing the likelihood of improved performance by

growth equities relative to value equities, expecting an increase in assets

under management subject to performance fees and a related increase in

seasonal volatility, indicating anticipated expense

levels, estimating the impact a clerical error may have on our earnings, and

anticipating the recovery of most of the cost of this error. The actual

performance of financial markets generally, how our performance measures against

that of our competitors, and other factors we cannot control will affect our

asset inflows and whether performance by growth equities relative to value

equities improves. Performance-based fees are by nature seasonal and volatile

and thus difficult to predict. Our expense levels in future periods depend

in

part on headcount and office space needed in response to the growth in volume,

complexity and global nature of our firm. The estimate of the impact of the

clerical error is based on very preliminary data. Accordingly, the estimated

impact on earnings may prove inaccurate as we gather and analyze additional

information. In addition, our ability to recover most of the cost of the error

is dependent, in part, on the availability of funds from the related

class-action settlement fund, the amount of which is not known, and the

willingness of our insurers to reimburse us under existing policies for this

cost.

|

Section

7.

|

Regulation

FD

|

|

Item

7.01.

|

Regulation

FD Disclosure.

|

AllianceBernstein

Holding is furnishing the 4Q06 Earnings Release, which is attached hereto as

Exhibit 99.01.

AllianceBernstein

Holding is furnishing the 4Q06 Review, which is attached hereto as Exhibit

99.02.

AllianceBernstein

Holding is furnishing the 4Q06 Transcript, which is attached hereto as Exhibit

99.03.

|

Section

9.

|

Financial

Statements and

Exhibits

|

|

Item

9.01.

|

Financial

Statements and Exhibits.

|

|

(d)

|

Exhibits.

|

|

4Q06

Earnings Release.

|

|

4Q06

Review.

|

|

4Q06

Transcript.

|

SIGNATURES

Pursuant

to the requirements of the Securities Exchange Act of 1934, the registrant

has

duly caused this report to be signed on its behalf by the undersigned thereunto

duly authorized.

|

ALLIANCEBERNSTEIN

HOLDING

L.P.

|

|||

|

Dated:

January 25, 2007

|

By:

|

/s/

Robert H. Joseph, Jr.

|

|

|

Robert

H. Joseph, Jr.

|

|||

|

Senior

Vice President and

|

|||

|

Chief

Financial Officer

|

|||

| |

Philip

Talamo, Investor Relations

212.969.2383

ir@alliancebernstein.com

|

John

Meyers, Media

212.969.2301

pr@alliancebernstein.com

|

News

Release

AllianceBernstein

Holding L.P. Announces Fourth Quarter Diluted Net Income of $1.48 per Unit

and

Declares a $1.48 per Unit Cash Distribution

New

York, NY, January 24, 2007

-

AllianceBernstein Holding L.P. (“AllianceBernstein Holding”) (NYSE: AB) and

AllianceBernstein L.P. (“AllianceBernstein”) today reported financial and

operating results for the quarter and full year ended December 31,

2006.

AllianceBernstein

Holding (The Publicly Traded Partnership):

|

·

|

Diluted

net income per Unit

for the quarter ended December 31, 2006 was $1.48, an increase

of 45.1%

from $1.02 for

the same period in 2005. Diluted net income per Unit for full year

2006

was $4.02, up from $3.02 in 2005.

|

|

·

|

Distribution

per Unit

for the fourth quarter of 2006 will be $1.48, an increase of 45.1%

from

$1.02 for the same period in 2005. The distribution is payable

on February

15, 2007 to holders of AllianceBernstein Holding Units at the close

of

business on February 5, 2007. Total distributions per Unit for

full year

2006 will be $4.02, up from $3.00 for full year

2005.

|

AllianceBernstein

(The Operating Partnership):

|

·

|

Assets

Under Management (AUM)

at

December 31, 2006 were $716.9 billion, a 23.9% increase from a

year ago,

due to market appreciation and net inflows across all distribution

channels.

|

|

·

|

Net

inflows for the three months

ended December 31, 2006 were $10.6 billion, consisting of Institutional

Investments net inflows of $6.3 billion, Retail net inflows of

$2.3

billion and Private Client net inflows of $2.0

billion.

|

|

·

|

Net

inflows

(1)

for the twelve months

ended December 31, 2006 were $47.8 billion, consisting of Institutional

Investments net inflows of $27.2 billion, Retail net inflows of

$12.2

billion and Private Client net inflows of $8.4

billion.

|

____________________

|

(1)

|

Excludes

acquisition of Hong Kong joint venture interest,

and transfers of certain client accounts among distribution channels

resulting from changes in how these accounts are serviced by

the

firm.

|

“On

the

most important metric, investment results for our clients, 2006 was a mixed

year. Returns in value equity services were extremely strong, with most non-U.S.

and global value services exceeding benchmarks by substantial margins. Fixed

income returns were far lower in absolute terms but were, in general, above

benchmarks as well, in some cases substantially. Growth services were the

exception, the relative performance of which was weak, especially in the

U.S.

The headwinds faced by this style of equity management continued to blow

strongly throughout the year, adversely affecting the returns in our growth

services. The gap in valuation between growth and value equities has now

declined to a level that suggests continued pressure on growth performance

is

nearing an end. We believe that our growth services are positioned to benefit

from this changing condition,” said Lewis Sanders, Chairman and Chief Executive

Officer.

“The

company’s organic growth rate was strong in the fourth quarter and for all 2006.

Net asset inflows for the year totaled $47.8 billion, an 8.3% annual rate.

All

client groups contributed to this growth, with flows in our U.S. retail mutual

fund and managed account business showing the most improvement compared with

2005.

“Assets

under management in global and international services grew by 50% for the

full

year and accounted for 54% of AUM at year end 2006. Growth in AUM for non-U.S.

clients remained very strong as well, at 44% for the full year, driving non-U.S.

client share of total AUM to 36% by year’s end.

“Revenue

in our institutional research services grew modestly in the fourth quarter,

resulting in a full year increase of 6%. However, after adjusting for the

reclassification from investment advisory fees to institutional research

services of transaction charges associated with investment management clients,

which declined significantly from 2005 levels, the increase in revenue was

approximately 16%. Market share improved as a function of continued strong

growth in algorithmic trading volumes in the U.S. and increased client

acceptance of our research services domestically and in our London-based

operations.

“Financial

results for the operating partnership overall were strong in 2006, with revenue

rising by 23.0%, net earnings rising by 33.9%, and operating margins expanding

by 290 basis points to 30.9%. Fourth quarter earnings grew by 45.4%, exceeding

expectations, a function primarily of very strong performance-related fees,

reflecting excellent results for our clients and strong growth in assets

under

management subject to such fees.

|

www.alliancebernstein.com

|

2

of

9

|

“We

recently discovered a clerical error made while processing claims for

class-action settlement proceeds on behalf of certain of our clients, including

some AllianceBernstein-sponsored mutual funds. Based on preliminary data,

we

believe the cost of this error could be on the order of $0.15 per Unit, most

of

which we anticipate will be recovered from residual settlement proceeds and/or

insurance. As more complete information on the cost of this error becomes

available, permitting us to establish a reserve, an adjustment to fourth

quarter

2006 earnings may be required.

“Continued

advances in revenue and earnings for the firm are dependent on meeting the

needs

of our clients, as measured by investment returns and superior service, the

achievement of which remains our primary focus,” concluded Mr. Sanders.

CONFERENCE

CALL INFORMATION RELATING TO FOURTH QUARTER 2006 RESULTS

JANUARY

24, 2007 AT 5:00 P.M. (Eastern

Standard Time)

AllianceBernstein’s

management will review fourth quarter 2006 financial and operating results

on

Wednesday, January 24, 2007, during a conference call beginning

at 5:00 p.m.

(EST),

following the release of its financial results after the close of the New

York

Stock Exchange. The conference call will be hosted by Lewis A. Sanders, Chairman

and Chief Executive Officer, and Gerald M. Lieberman, President and Chief

Operating Officer.

Parties

may access the conference call by either telephone or webcast.

|

1.

|

To

listen by telephone, please dial 888-694-4676 in the U.S. or 973-582-2737

outside the U.S., ten minutes before the 5:00 p.m. (EST)

scheduled start time. The conference ID# is

8315265.

|

|

2.

|

To

listen by webcast, please visit AllianceBernstein’s Investor Relations

website at http://ir.alliancebernstein.com at least fifteen minutes

prior

to the call to download and install any necessary audio

software.

|

The

presentation slides that will be reviewed during the conference call are

expected to be available on AllianceBernstein’s website at the above web address

after the release of its results on January 24, 2007.

An

audio

replay of the conference call will be made available for one week beginning

at

7:00 p.m. (EST)

on

January 24, 2007. In the U.S., please call (877) 519-4471 or, outside the

U.S.,

call (973) 341-3080, and provide the conference ID# 8315265. The replay will

also be available via webcast on AllianceBernstein’s website for one

week.

About

AllianceBernstein

AllianceBernstein

is a leading global investment management firm providing investment management

services for many of the largest U.S. public and private employee benefit

plans,

foundations, public employee retirement funds, pension funds, endowments,

banks,

insurance companies and high-net-worth individuals worldwide. AllianceBernstein

is also one of the largest mutual fund sponsors, with a diverse family of

globally distributed mutual fund portfolios. Through its subsidiary, Sanford

C.

Bernstein & Co., LLC, AllianceBernstein provides in-depth research,

portfolio strategy and trade execution to the institutional investment

community.

|

www.alliancebernstein.com

|

3

of

9

|

At

December 31, 2006, AllianceBernstein Holding owned approximately 33.1% of

the

issued and outstanding AllianceBernstein Units. AXA Financial was the beneficial

owner of approximately 59.9% of the AllianceBernstein Units at December 31,

2006

(including those held indirectly through its ownership of approximately 1.7%

of

the issued and outstanding Holding Units) which, including the general

partnership interests in AllianceBernstein and Holding, represent an approximate

60.3% economic interest in AllianceBernstein. AXA Financial is a wholly-owned

subsidiary of AXA, one of the largest global financial services

organizations.

Forward-Looking

Statements

Certain

statements in this news release are “forward-looking statements” within the

meaning of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements are subject to risks, uncertainties, and other

factors that could cause actual results to differ materially from future

results

expressed or implied by such forward-looking statements. The most significant

of

these factors include, but are not limited to, the following: the performance

of

financial markets, the investment performance we achieve for our clients,

general economic conditions, future acquisitions, competitive conditions,

and

government regulations, including changes in tax rates. We caution readers

to

carefully consider our forward-looking statements in light of these factors.

Further, these forward-looking statements speak only as of the date on which

such statements are made; we undertake no obligation to update any

forward-looking statements to reflect subsequent events or circumstances.

For

further information regarding these forward-looking statements and the factors

that could cause actual results to differ, see “Risk Factors” in Item 1 of Form

10-K for the year ended December 31, 2005. Any or all of the forward-looking

statements that we make in Form 10-K, this news release, or any other public

statements we issue may turn out to be wrong. Of

course, factors other than those listed in “Risk Factors” could also adversely

affect our revenues, financial condition, results of operations, and business

prospects.

The

forward-looking statements referred to in the preceding paragraph include

statements regarding an end to pressure on investment returns of growth equities

relative to value equities, and our belief that our growth services are

positioned to benefit from this changing condition. The actual performance

of

financial markets and other factors beyond our control will affect our

investment success.

|

www.alliancebernstein.com

|

4

of

9

|

ALLIANCEBERNSTEIN

L.P.

(THE

OPERATING PARTNERSHIP)

SUMMARY

CONSOLIDATED STATEMENTS OF INCOME

DECEMBER

31, 2006

(unaudited,

in thousands)

|

Three

Months Ended

|

Twelve

Months Ended

|

||||||||||||

|

12/31/06

|

12/31/05

|

12/31/06

|

12/31/05

|

||||||||||

|

Revenues:

|

|||||||||||||

|

Investment

Advisory & Services Fees

|

$

|

895,383

|

$

|

667,773

|

$

|

2,890,229

|

$

|

2,259,392

|

|||||

|

Distribution

Revenues

|

109,949

|

97,066

|

421,045

|

397,800

|

|||||||||

|

Institutional

Research Services

|

88,769

|

87,103

|

375,075

|

352,757

|

|||||||||

|

Dividend

and Interest Income

|

86,050

|

55,677

|

266,520

|

152,781

|

|||||||||

|

Investment

Gains (Losses)

|

23,871

|

5,401

|

53,134

|

28,631

|

|||||||||

|

Other

Revenues

|

32,923

|

29,088

|

132,237

|

117,227

|

|||||||||

|

Total

Revenues

|

1,236,945

|

942,108

|

4,138,240

|

3,308,588

|

|||||||||

|

Less:

Interest Expense

|

50,247

|

31,522

|

187,833

|

95,863

|

|||||||||

|

Net

Revenues

|

1,186,698

|

910,586

|

3,950,407

|

3,212,725

|

|||||||||

|

Expenses:

|

|||||||||||||

|

Employee

Compensation & Benefits

|

427,845

|

341,182

|

1,547,627

|

1,262,198

|

|||||||||

|

Promotion

& Servicing:

|

|||||||||||||

|

Distribution

Plan Payments

|

77,632

|

67,009

|

292,886

|

291,953

|

|||||||||

|

Amortization

of Deferred Sales Commissions

|

28,721

|

28,836

|

100,370

|

131,979

|

|||||||||

|

Other

|

57,359

|

51,359

|

218,944

|

198,004

|

|||||||||

|

General

& Administrative

|

140,975

|

109,451

|

527,296

|

384,339

|

|||||||||

|

Interest

on Borrowings

|

2,905

|

6,249

|

23,124

|

25,109

|

|||||||||

|

Amortization

of Intangible Assets

|

5,178

|

5,175

|

20,710

|

20,700

|

|||||||||

|

740,615

|

609,261

|

2,730,957

|

2,314,282

|

||||||||||

|

Operating

Income

|

446,083

|

301,325

|

1,219,450

|

898,443

|

|||||||||

|

Non-Operating

Income

|

3,903

|

10,227

|

20,196

|

34,446

|

|||||||||

|

Income

before Income Taxes

|

449,986

|

311,552

|

1,239,646

|

932,889

|

|||||||||

|

Income

Taxes

|

28,557

|

21,666

|

76,568

|

64,571

|

|||||||||

|

NET

INCOME

|

$

|

421,429

|

$

|

289,886

|

$

|

1,163,078

|

$

|

868,318

|

|||||

|

Operating

income margin

|

37.6

|

%

|

33.1

|

%

|

30.9

|

%

|

28.0

|

%

|

|||||

|

www.alliancebernstein.com

|

5

of

9

|

ALLIANCEBERNSTEIN

HOLDING L.P.

(THE

PUBLICLY TRADED PARTNERSHIP)

SUMMARY

STATEMENTS OF INCOME

(unaudited,

in thousands except per unit amounts)

|

Three

Months Ended

|

Twelve

Months Ended

|

||||||||||||

|

12/31/06

|

12/31/05

|

12/31/06

|

12/31/05

|

||||||||||

|

Equity

in Earnings of Operating Partnership

|

$

|

137,592

|

$

|

92,143

|

$

|

377,298

|

$

|

275,054

|

|||||

|

Income

Taxes

|

10,334

|

7,607

|

34,473

|

26,990

|

|||||||||

|

NET

INCOME

|

127,258

|

84,536

|

342,825

|

248,064

|

|||||||||

|

Additional

Equity in Earnings of Operating Partnership (1)

|

2,161

|

1,292

|

5,581

|

3,326

|

|||||||||

|

NET

INCOME - Diluted (2)

|

$

|

129,419

|

$

|

85,828

|

$

|

348,406

|

$

|

251,390

|

|||||

|

DILUTED

NET INCOME PER UNIT

|

$

|

1.48

|

$

|

1.02

|

$

|

4.02

|

$

|

3.02

|

|||||

|

|

|

|

|

||||||||||

|

DISTRIBUTION

PER UNIT

|

$

|

1.48

|

$

|

1.02

|

$

|

4.02

|

$

|

3.00

|

|||||

|

(1)

|

To

reflect higher ownership in the Operating Partnership resulting

from

application of the treasury stock method to outstanding

options.

|

|

(2)

|

For

calculation of Diluted Net Income per

Unit.

|

ALLIANCEBERNSTEIN

AND ALLIANCEBERNSTEIN HOLDING

UNITS

OUTSTANDING AND WEIGHTED AVERAGE UNITS OUTSTANDING

DECEMBER

31, 2006

|

Weighted

Average Units

|

||||||||||||||||

|

Three

Months Ended

|

Twelve

Months Ended

|

|||||||||||||||

|

Period

End

|

||||||||||||||||

|

Units

|

Basic

|

Diluted

|

Basic

|

Diluted

|

||||||||||||

|

AllianceBernstein

|

259,062,014

|

258,573,531

|

260,889,296

|

257,718,845

|

259,961,614

|

|||||||||||

|

AllianceBernstein

Holding

|

85,668,171

|

85,179,688

|

87,495,453

|

84,325,002

|

86,567,771

|

|||||||||||

|

www.alliancebernstein.com

|

6

of

9

|

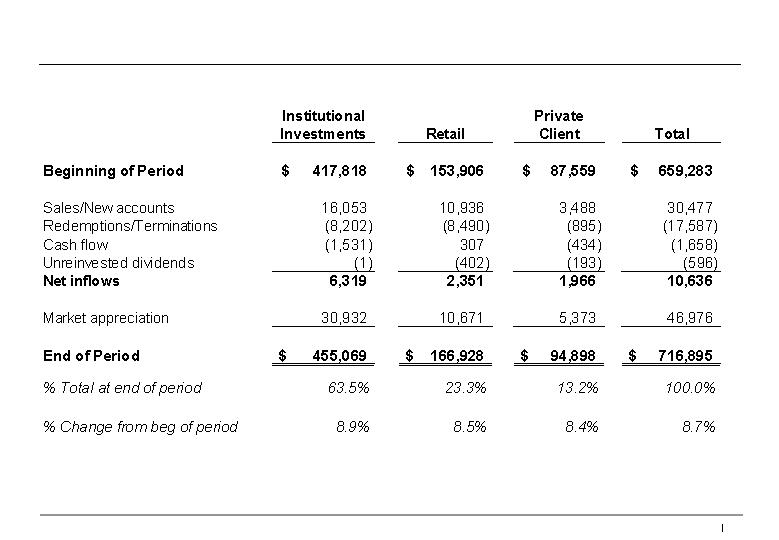

ALLIANCEBERNSTEIN

L.P.

ASSETS

UNDER MANAGEMENT

THREE

MONTHS ENDED DECEMBER 31, 2006

($

millions)

|

|

Institutional

|

|

Private

|

|

|||||||||

|

|

Investments

|

Retail

|

Client

|

Total

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Beginning

of Period

|

$

|

417,818

|

$

|

153,906

|

$

|

87,559

|

$

|

659,283

|

|||||

|

|

|

|

|

|

|||||||||

|

Sales/New

accounts

|

16,053

|

10,936

|

3,488

|

30,477

|

|||||||||

|

Redemptions/Terminations

|

(8,202

|

)

|

(8,490

|

)

|

(895

|

)

|

(17,587

|

)

|

|||||

|

Cash

flow

|

(1,531

|

)

|

307

|

(434

|

)

|

(1,658

|

)

|

||||||

|

Unreinvested

dividends

|

(1

|

)

|

(402

|

)

|

(193

|

)

|

(596

|

)

|

|||||

|

Net

inflows

|

6,319

|

2,351

|

1,966

|

10,636

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Market

appreciation

|

30,932

|

10,671

|

5,373

|

46,976

|

|||||||||

|

|

|

|

|

|

|||||||||

|

End

of Period

|

$

|

455,069

|

$

|

166,928

|

$

|

94,898

|

$

|

716,895

|

|||||

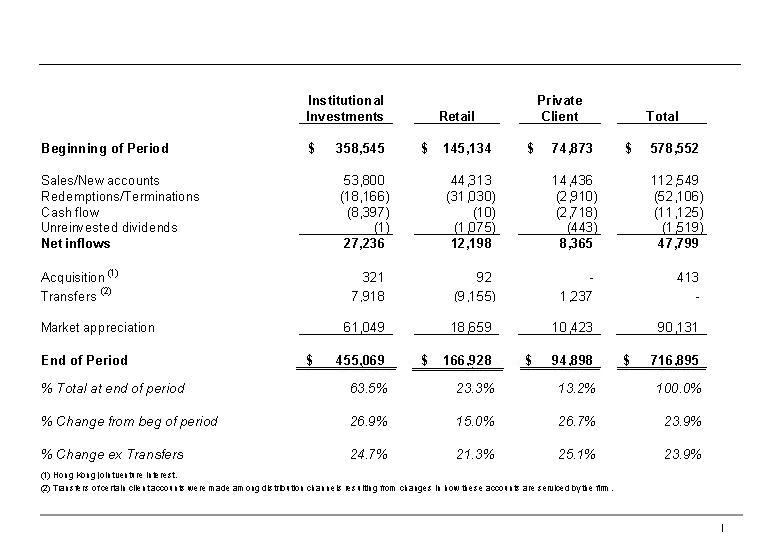

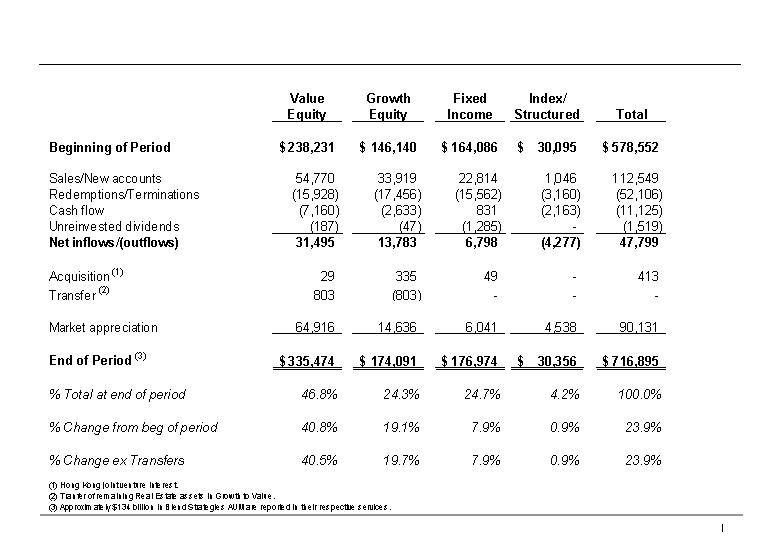

ALLIANCEBERNSTEIN

L.P.

ASSETS

UNDER MANAGEMENT

TWELVE

MONTHS ENDED DECEMBER 31, 2006

($

millions)

|

|

Institutional

|

|

Private

|

|

|||||||||

|

|

Investments

|

Retail

|

Client

|

Total

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Beginning

of Period

|

$

|

358,545

|

$

|

145,134

|

$

|

74,873

|

$

|

578,552

|

|||||

|

|

|

|

|

|

|||||||||

|

Sales/New

accounts

|

53,800

|

44,313

|

14,436

|

112,549

|

|||||||||

|

Redemptions/Terminations

|

(18,166

|

)

|

(31,030

|

)

|

(2,910

|

)

|

(52,106

|

)

|

|||||

|

Cash

flow

|

(8,397

|

)

|

(10

|

)

|

(2,718

|

)

|

(11,125

|

)

|

|||||

|

Unreinvested

dividends

|

(1

|

)

|

(1,075

|

)

|

(443

|

)

|

(1,519

|

)

|

|||||

|

Net

inflows

|

27,236

|

12,198

|

8,365

|

47,799

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Acquisition

(1)

|

321

|

92

|

-

|

413

|

|||||||||

|

Transfers

(2)

|

7,918

|

(9,155

|

)

|

1,237

|

-

|

||||||||

|

|

|

|

|

|

|||||||||

|

Market

appreciation

|

61,049

|

18,659

|

10,423

|

90,131

|

|||||||||

|

|

|

|

|

|

|||||||||

|

End

of Period

|

$

|

455,069

|

$

|

166,928

|

$

|

94,898

|

$

|

716,895

|

|||||

|

(1)

|

Acquisition

of Hong Kong joint venture

interest.

|

|

(2)

|

Transfer

of certain client accounts were made among distribution channels

resulting

from changes in how these accounts are serviced by the

firm.

|

|

www.alliancebernstein.com

|

7

of

9

|

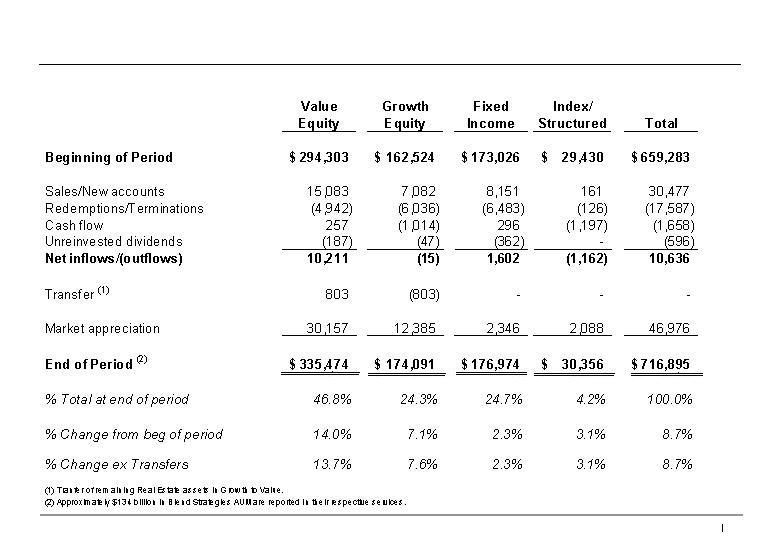

ALLIANCEBERNSTEIN

L.P.

ASSETS

UNDER MANAGEMENT

BY

INVESTMENT SERVICE

AT

DECEMBER 31, 2006

($

millions)

|

|

Institutional

Investments

|

Retail

|

Private

Client

|

Total

|

|||||||||

|

Equity:

|

|

|

|

|

|||||||||

|

Growth

|

|

|

|

|

|||||||||

|

U.S.

|

$

|

36,670

|

$

|

28,587

|

$

|

13,237

|

$

|

78,494

|

|||||

|

Global

& International

|

66,242

|

19,937

|

9,418

|

95,597

|

|||||||||

|

|

102,912

|

48,524

|

22,655

|

174,091

|

|||||||||

|

Value

|

|

|

|

|

|||||||||

|

U.S.

|

55,562

|

35,749

|

27,703

|

119,014

|

|||||||||

|

Global

& International

|

158,572

|

38,797

|

19,091

|

216,460

|

|||||||||

|

|

214,134

|

74,546

|

46,794

|

335,474

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Total

Equity

|

317,046

|

123,070

|

69,449

|

509,565

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Fixed

Income:

|

|

|

|

|

|||||||||

|

U.S.

|

73,414

|

11,420

|

25,032

|

109,866

|

|||||||||

|

Global

& International

|

39,166

|

27,614

|

328

|

67,108

|

|||||||||

|

|

112,580

|

39,034

|

25,360

|

176,974

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Index/Structured:

|

|

|

|

|

|||||||||

|

U.S.

|

19,942

|

4,824

|

80

|

24,846

|

|||||||||

|

Global

& International

|

5,501

|

-

|

9

|

5,510

|

|||||||||

|

|

25,443

|

4,824

|

89

|

30,356

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Total:

|

|

|

|

|

|||||||||

|

U.S.

|

185,588

|

80,580

|

66,052

|

332,220

|

|||||||||

|

Global

& International

|

269,481

|

86,348

|

28,846

|

384,675

|

|||||||||

|

|

$

|

455,069

|

$

|

166,928

|

$

|

94,898

|

$

|

716,895

|

|||||

|

www.alliancebernstein.com

|

8

of

9

|

ALLIANCEBERNSTEIN

L.P.

ASSETS

UNDER MANAGEMENT

($

millions)

|

|

Three

Month Period

|

Twelve

Month Period

|

|||||||||||

|

|

12/31/06

|

12/31/05

|

12/31/06

|

12/31/05

|

|||||||||

|

|

|

|

|

|

|||||||||

|

Ending

Assets Under Management

|

$

|

716,895

|

$

|

578,552

|

$

|

716,895

|

$

|

578,552

|

|||||

|

|

|

|

|

|

|||||||||

|

Average

Assets Under Management

|

$

|

689,225

|

$

|

563,024

|

$

|

640,966

|

$

|

541,159

|

|||||

ALLIANCEBERNSTEIN

L.P.

ASSETS

UNDER MANAGEMENT

BY

CLIENT DOMICILE

AT

DECEMBER 31, 2006

($

millions)

|

|

Institutional

Investments

|

Retail

|

Private

Client

|

Total

|

|||||||||

|

|

|

|

|

|

|||||||||

|

U.S.

Clients

|

$

|

241,044

|

$

|

126,674

|

$

|

92,388

|

$

|

460,106

|

|||||

|

Non-U.S.

Clients

|

214,025

|

40,254

|

2,510

|

256,789

|

|||||||||

|

|

$

|

455,069

|

$

|

166,928

|

$

|

94,898

|

$

|

716,895

|

|||||

|

www.alliancebernstein.com

|

9

of

9

|

Fourth-Quarter

2006

Review

AllianceBernstein

Fourth

Quarter

2006 Review

Gerald

M.

Lieberman

President

&

Chief Operating Officer

Lewis

A.

Sanders

Chairman

&

Chief

Executive Officer

Any

forecasts in this material may not be realized. Information or opinions

should

not be construed as investment advice.

January

24,

2007

1

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Forward-Looking

Statements

Certain

statements in this presentation and the accompanying oral remarks are

“forward-looking statements” within the meaning of the Private Securities

Litigation Reform Act of 1995. These forward-looking statements are

subject to risks, uncertainties, and other factors that could cause actual

results to differ materially from future results expressed or implied

by such

forward-looking statements. The most significant of these factors include,

but

are not limited to, the following: the performance of financial markets;

the

investment performance we achieve for our clients; general economic conditions;

future acquisitions; competitive conditions; and government regulations,

including changes in tax rates. We caution readers to carefully consider

our forward-looking statements in light of these factors. Further, these

forward-looking statements speak only as of the date on which such statements

are made; we undertake no obligation to update any forward-looking statements

to

reflect subsequent events or circumstances. For further information

regarding these forward-looking statements and the factors that could

cause

actual results to differ, see “Risk Factors” in Item 1 of Form 10-K for the year

ended December 31, 2005. Any or all of the forward-looking statements that

we make in Form 10-K, this news release, or any other public statements

we issue

may turn out to be wrong. Of course, factors other than those listed

in “Risk

Factors” could also adversely affect our revenues, financial condition, results

of operations, and business prospects.

The

oral remarks accompanying this presentation include forward looking statements

predicting increases in net asset inflows, describing the likelihood

of improved

performance by growth equities relative to value equities, expecting

an increase

in assets under management subject to performance fees and a related

increase in

seasonal volatility, and indicating anticipated expense levels. The actual

performance of financial markets generally, how our performance measures

against

that of our competitors, and other factors we cannot control will affect

our

asset inflows and whether performance by growth equities relative to

value

equities improves. Performance-based fees are by nature seasonal and

volatile

and thus difficult to predict. Our expense levels in future periods depend

in part on headcount and office space needed in response to the growth

in

volume, complexity and global nature of our firm.

In

light of

Regulation FD, management will be limited in responding to inquiries

from

investors or analysts in a non-public forum.

Introduction

2

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

<

Capital

markets

strong

<

Relative

performance

somewhat mixed, but with substantial exceptions

<

Strong

market

appreciation and net AUM inflows across all channels

<

Summary

of financial

performance vs. 4Q05

=

AllianceBernstein

(Operating)

Ø

Net

Revenues up

30.3%

Ø

Operating

Income up

48.0%

Ø

Net

Income up

45.4%

=

AllianceBernstein

Holding distribution of $1.48 per Unit up 45.1%

<

Administrative

error

may result in an adjustment to fourth quarter earnings on the order of

$0.15 per

Unit; substantial recovery of this amount is anticipated

AllianceBernstein

– Fourth Quarter Highlights

3

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

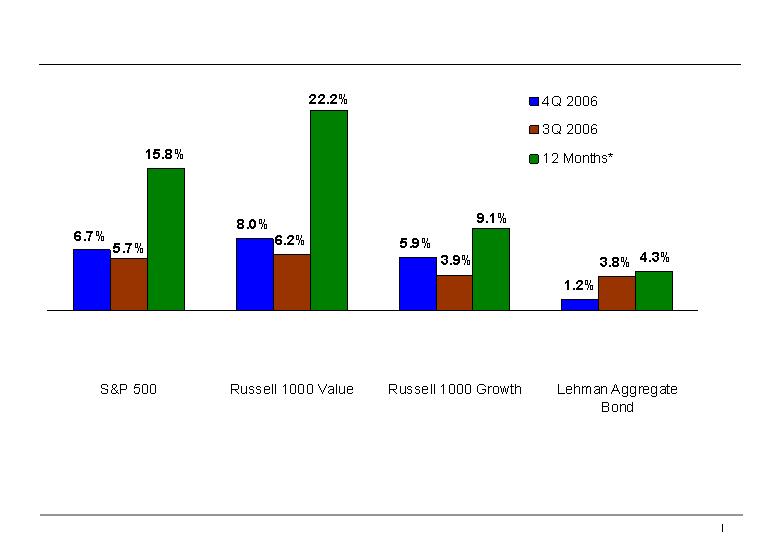

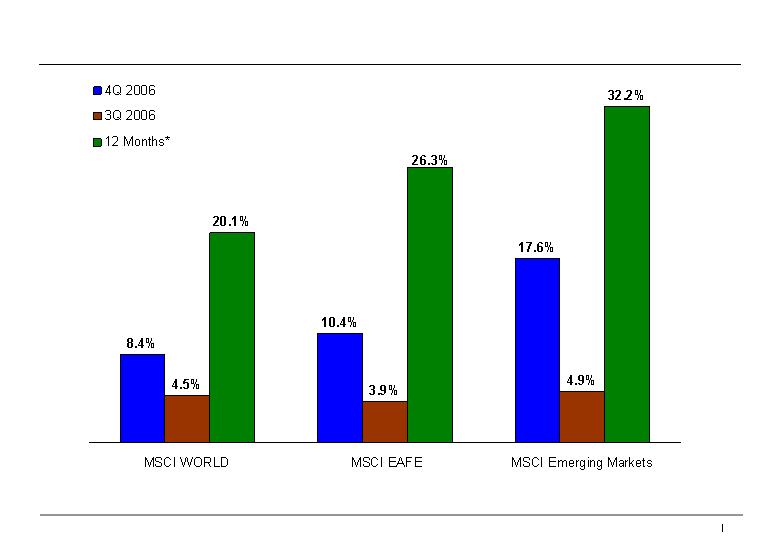

*12

months ending December 31, 2006.

Source:

Frank Russell Company, Standard & Poor’s, and Lehman

Brothers.

Market

Performance - U.S.

4

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

*12

months ending December 31, 2006.

Source:

MSCI (Morgan Stanley Capital International).

Market

Performance - Non-U.S.

5

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

<

Value

Equities

performance was very strong

<

Fixed

Income

outperformed, in some cases substantially

<

Growth

Equities

performance generally weak, but turnaround expected

Relative

Performance Summary

6

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Three

Months

Ended December 31, 2006

In

$ Millions

Changes

in

Assets Under Management

By

Channel

7

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Twelve

Months Ended December 31, 2006

In

$

Millions

Changes

in

Assets Under Management

By

Channel

8

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Three

Months

Ended December 31, 2006

In

$

Millions

Changes

in

Assets Under Management

By

Investment Service

9

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Twelve

Months Ended December 31, 2006

In

$

Millions

Changes

in

Assets Under Management

By

Investment Service

10

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

(1)

Transfers of certain client accounts were made among distribution channels

resulting from changes in how these accounts are serviced by the firm.

<

Value

Equity and

Blend Strategies services accounted

for roughly 70% of all new

assets

for roughly 70% of all new

assets

<

Global

&

International services comprised approximately 75% of all new assets

<

Pipeline

of won but

unfunded new mandates remains strong

Institutional

Investments—

Fourth

Quarter Highlights

11

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

(1)Transfers

of certain client accounts were made among distribution channels resulting

from

changes in how these accounts are serviced by the firm.

<

Positive

net inflows

for sixth consecutive quarter

<

Significant

increase

in net asset inflows for full year in:

=

U.S.

Retail mutual

funds

=

Global

&

International and Multi-Strategy services

<

Net

positive flows

in:

=

U.S.

and Luxembourg

funds

=

Equity

and fixed

income

Retail—

Fourth

Quarter Highlights

12

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

(1)Transfers

of certain client accounts were made among distribution channels resulting

from

changes in how these accounts are serviced by the firm.

Private

Client—

Fourth

Quarter Highlights

<

Net

inflows

increased from the third quarter

<

Financial

Advisor

headcount increased to 298 – up 14.2%

from December 2005,

including the opening of our

U.K. office

from December 2005,

including the opening of our

U.K. office

13

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

<

Revenue

growth of

1.9% from prior year quarter and 6.3% for the full year

<

Revenue,

adjusted

for advisory fee reclassification, up 6.1% from prior year quarter and

16.2% for

the full year

<

4Q06

revenue growth

driven by London, with U.S. about flat

<

Client

use of our

algorithmic trading platform in the U.S. continues to grow; on schedule

for 1Q07

launch in Europe

<

Outstanding

results

in Institutional Investor’s “Best U.S. Independents”

survey:

=

Ranked

in 26

sectors, including first place finishes in 23 sectors

Institutional

Research Services—

Fourth

Quarter Highlights

14

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

By

Client

Domicile

By

Investment Service

In

$

Billions

Non-U.S.

UP

44%

Global

&

Int’l

UP

50%

$415

72%

$717

Billion

+24%

at

Dec 31,

2006

Equity

$579

Billion

at

Dec 31, 2005

$164

28%

$540

75%

$177

25%

F/I

Equity

F/I

Growth

in

Global Assets

15

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Blend

Strategies

Index/Structured

$30

Assets

Under

Management

by

Investment Service

$717

Billion

Blend

Strategies AUM

$134

Billion(1)

(+52%

vs.

12/31/05)

(1)

Includes approximately $4 billion of Blend Fixed Income AUM.

25%

38%

9%

9%

15%

4%

(1)

In

$

Billions

Growth

in

Blend Strategies Assets

16

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

(1)

Includes

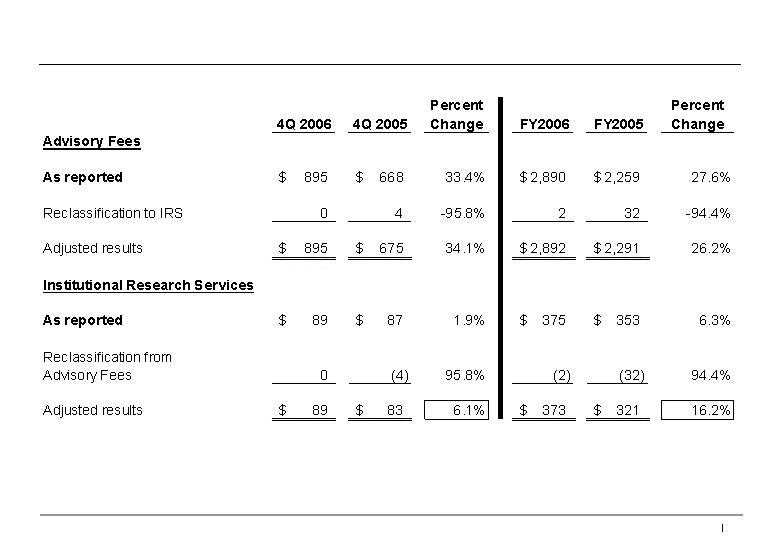

approximately $4 million reclassified from advisory fees.

(2)

Includes

Shareholder Servicing, Investment Gains (Losses) and Other Revenues.

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$

Millions

AllianceBernstein

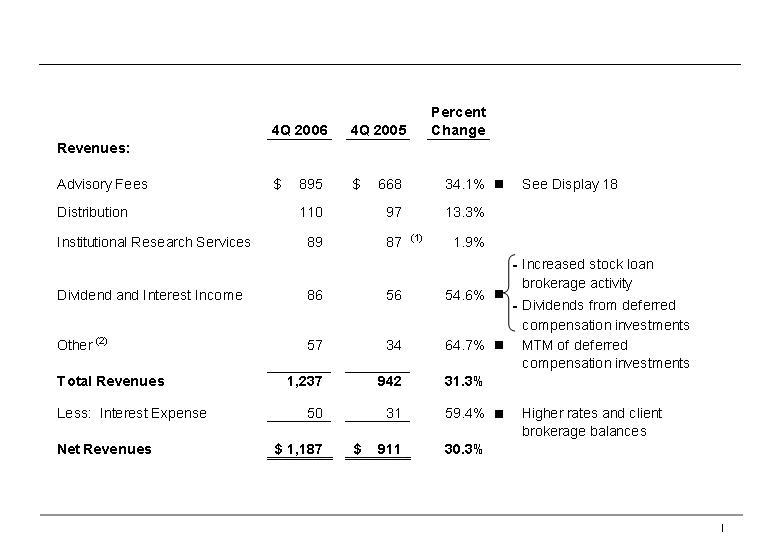

Fourth Quarter Revenues

17

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

AllianceBernstein

Fourth Quarter Advisory

Fees

18

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$

Millions

AllianceBernstein

Fourth Quarter Operating Expenses

19

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$

Millions

AllianceBernstein

Fourth Quarter Compensation &

Benefits

20

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$

Millions

AllianceBernstein

Fourth

Quarter Expenses

21

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

(1)

Includes $7 million gain on disposition of South Africa J.V.

(2)

Includes $7 million gain on disposition of South Africa J.V. and $8 million

gain

on disposition of Indian mutual funds

(3)

Operating Income as a percentage of net revenues.

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$

Millions

AllianceBernstein

Fourth Quarter Net Income

22

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

NOTE:

Percentages are calculated using revenues and expenses rounded to the

nearest

thousand.

In

$ Millions

(except per unit amounts)

AllianceBernstein

Holding Financial Results

23

Q&A

24

Appendix

25

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Market

Environment

26

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

Performance: Institutional Growth Equity (After

Fees)

(1)

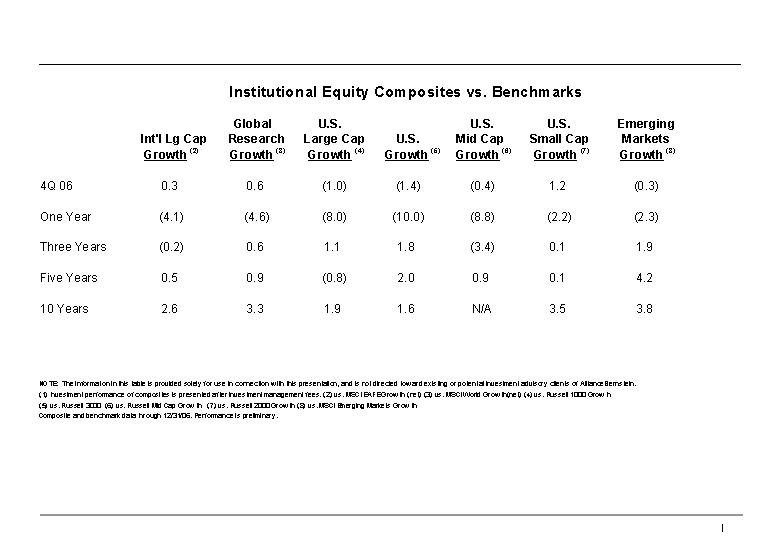

27

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

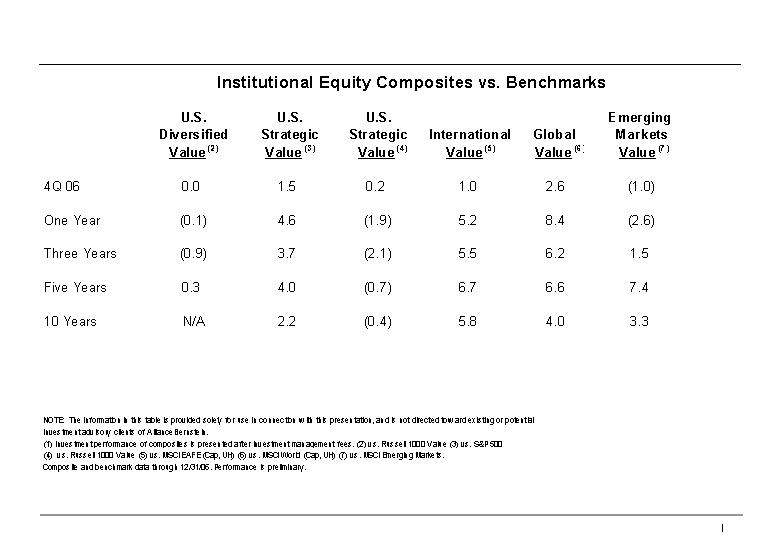

Relative

Performance: Institutional Value Equity (After

Fees) (1)

28

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

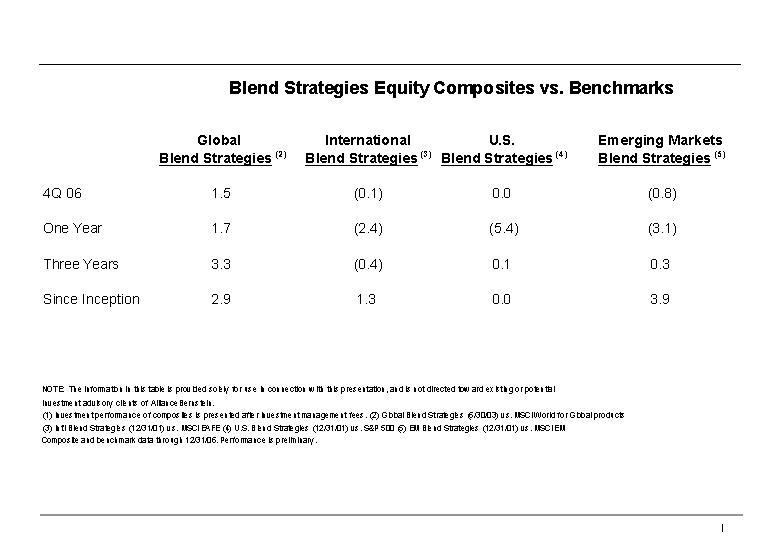

Performance: Blend Strategies Services (After

Fees)

(1)

29

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

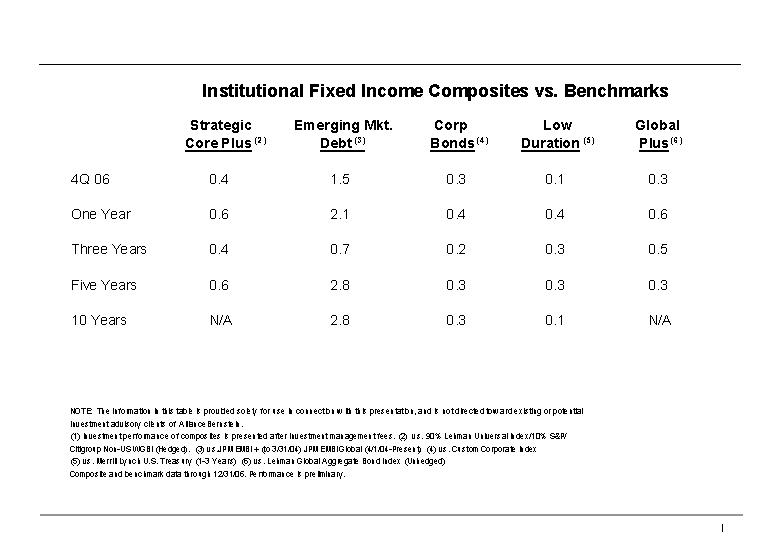

Performance: Institutional Fixed Income (After

Fees)

(1)

30

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Absolute

Performance: Private Client (After

Fees) (1)

31

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

Performance: Retail Growth Equity (After

Fees) (1)

32

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

Performance: Retail Value Equity (After

Fees) (1)

33

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

Performance: Retail Fixed Income (After

Fees) (1)

34

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Relative

Performance: Wealth Strategies (After

Fees) (1)

35

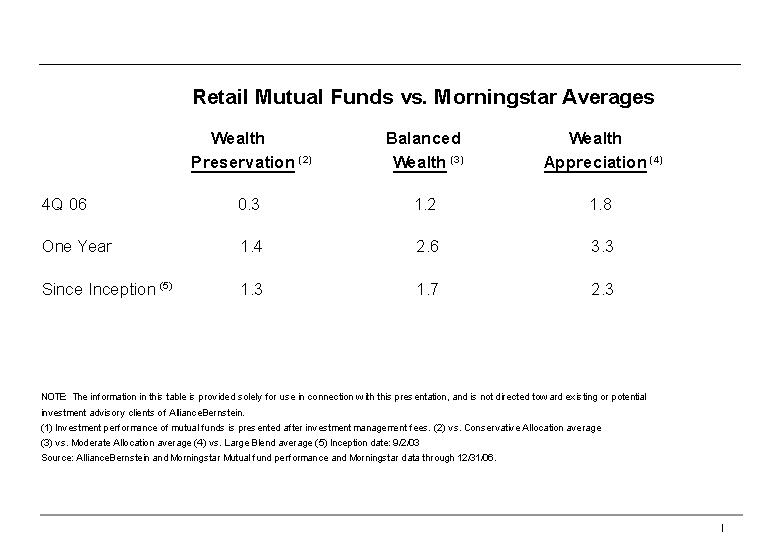

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

Bernstein

Value Equities

Inception

Date

Inception–

Dec

2006

Alliance

Growth Equities

Inception

Date

The

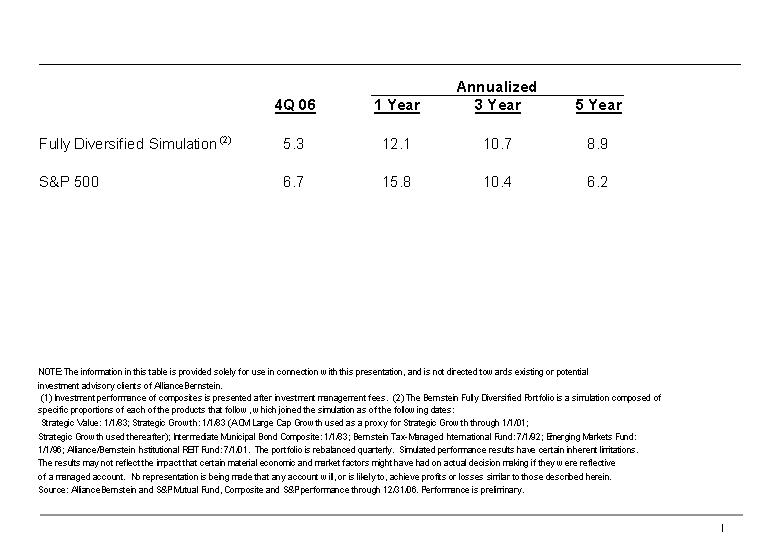

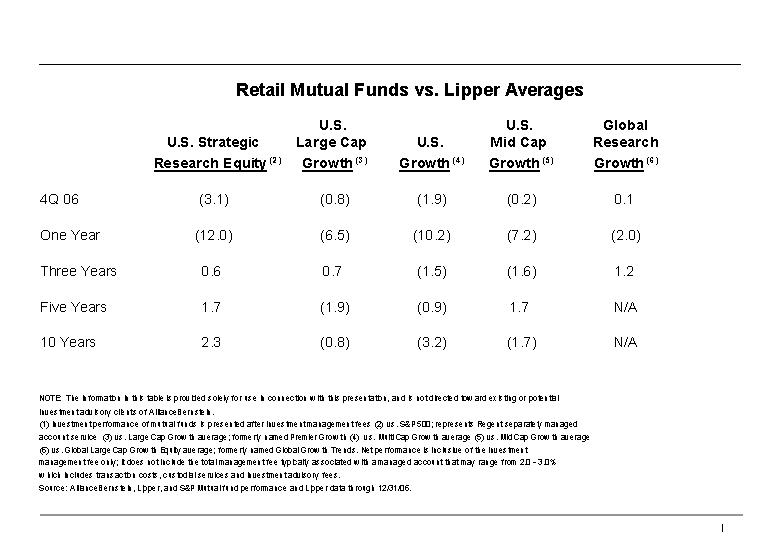

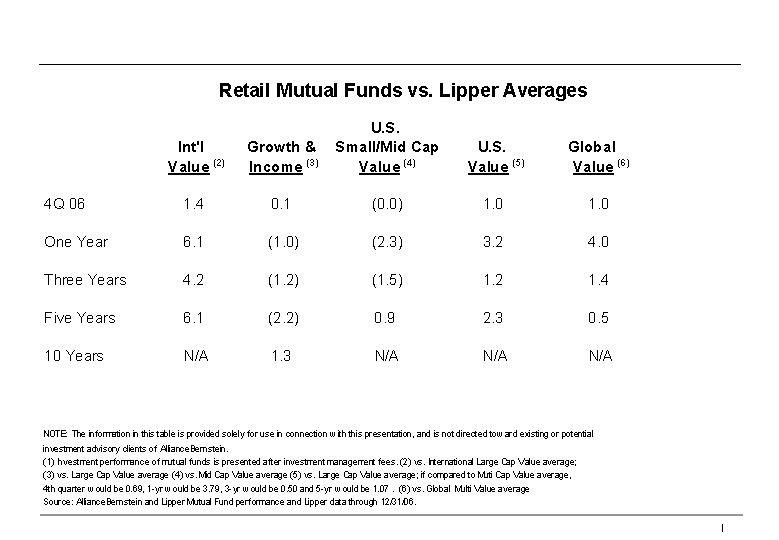

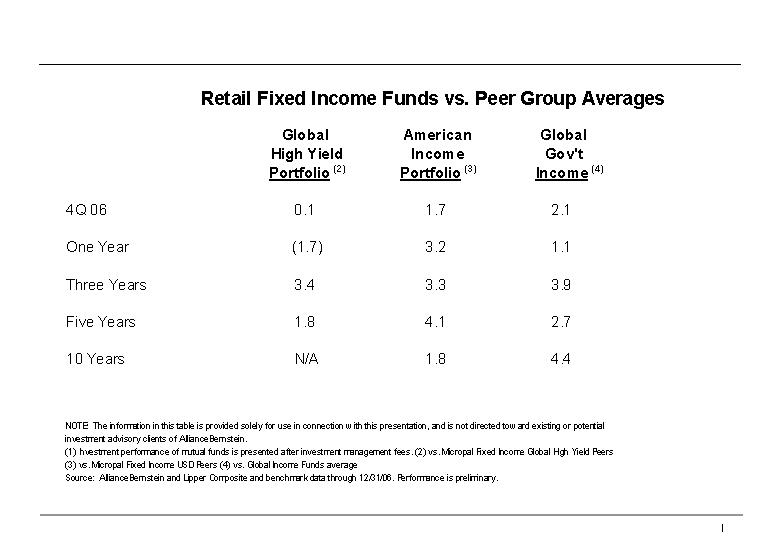

performance figures in AllianceBernstein Fixed Income reflect corrections

made

to the original presentation.

The

information in this table is provided solely for use in connection

with this

presentation and is not directed towards existing or potential investment

advisory clients of AllianceBernstein. Past performance is no guarantee

of

future results. Source: Bloomberg, Citigroup, FTSE, JPMorgan Chase,

Lehman

Brothers, Merrill Lynch, MSCI, Nomura, Russell Investment Group, Scotia

Capital,

S&P, TOPIX, and AllianceBernstein.

AllianceBernstein

Style Blend

AllianceBernstein

Fixed Income

Net-of-Fee

Annualized Relative Performance Premiums

Inception–

Dec

2006

Investment

Performance: Delivering Results for Clients

36

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

In

$ Millions

AllianceBernstein

Transaction Fees

37

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

In

$ Thousands,

Unaudited

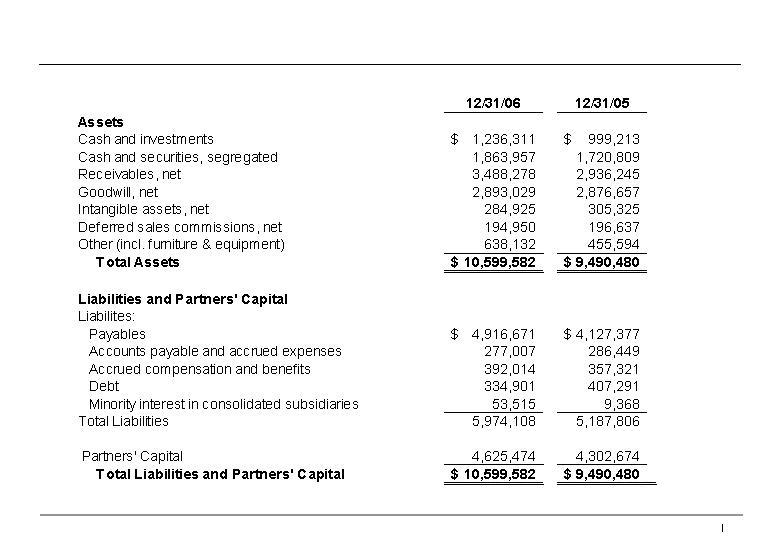

AllianceBernstein

Consolidated Balance Sheet

38

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

In

$ Thousands,

Unaudited

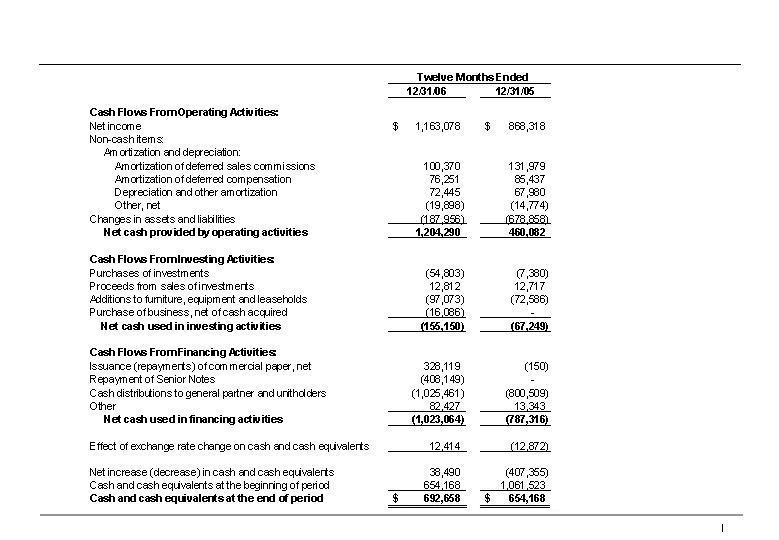

AllianceBernstein

Consolidated Statement of Cash Flows

39

Fourth-Quarter

2006

Review

Proprietary

–

For

AllianceBernstein L.P. use only

AllianceBernstein

AllianceBernstein®

and the AB AllianceBernstein Logo are trademarks and service marks owned

by

AllianceBernstein L.P.

40

Moderator:

Philip Talamo

January

24, 2007

5:00

p.m. EST

OPERATOR:

Thank you for standing by, and welcome to the AllianceBernstein fourth quarter

2006 earnings review. At this time all participants are in- listen only mode.

After the formal remarks there will be a question and answer session and

I will

give you instructions on how to ask a question at that time.

As

a

reminder, this conference is being recorded and will be archived for one

week. I

would now like to turn the conference over to the host for this call, the

Director of Investor Relations for AllianceBernstein, Mr. Philip Talamo.

Go

ahead.

PHILIP

TALAMO, DIRECTOR OF INVESTOR RELATIONS, ALLIANCEBERNSTEIN: Thank you, Lindsay.

Good afternoon everyone, and welcome to our fourth quarter Earnings Review.

As a

reminder, this conference call is being webcast and is supported by a slide

presentation that can be found on our web site at alliancebernstein.com.

Presenting

our results today is Jerry Lieberman, President and Chief Operating Officer.

Lew

Sanders, our Chairman and Chief Executive Officer and Bob Joseph, our CFO,

will

also be available to answer questions at the end of Jerry’s formal remarks.

I’d

like

to take this opportunity to note that some of the information we present

today

may be forward looking in nature, and as such is subject to certain SEC rules

and regulations regarding disclosure. Our disclosure regarding forward looking

statements can be found on page two of our slide presentation as well as

in the

risk factors section of our 2005 Form 10-K.

In

light

of the SEC’s regulation FD, management is limited in responding to inquiries

from investors and analysts in a non-public forum. Therefore, we encourage

you

to ask all questions of a material nature on this call.

At

this

time I’d like to turn the call over to Jerry Lieberman.

JERRY

LIEBERMAN, PRESIDENT AND COO, ALLIANCEBERNSTEIN: Thank you, Phil, and good

afternoon to everyone on the call. I’ll start today’s call with a few highlights

and then add some additional commentary and texture on the quarter and the

full

year.

Well

it

all starts with investment returns, and the capitals markets produced strong

gains globally, driven by a growing global economy and robust corporate

earnings. From a relative performance perspective, AllianceBernstein’s Value

Equity services continued to outperform their benchmarks and our Fixed Income

services continued their trend of improving performance.

Conversely,

performance in our Growth Equity services materially lagged their respective

benchmarks in the quarter and for the year, although the three, five and

ten

year period returns for these services remain generally competitive.

Our

firm’s organic growth rate was strong for the quarter and the year. We ended the

year with client assets under management of just under $717 billion, an increase

of 23.9 percent for the year, as market appreciation, performance and net

inflows added $138 billion to AUM.

Operating

partnership net revenues were nearly $1.2 billion for the quarter, up 30.3

percent versus fourth quarter ’05, with performance fees a significant

contributor. Operating income was up 48 percent and Net Income increased

by more

than 45 percent to a record $421 million.

Net

income and distribution per unit for AllianceBernstein Holding, the publicly

traded partnership, were a record $1.48, up 45.1 percent versus the fourth

quarter of 2005.

1

Finally,

there is a very recent development that we mentioned in our press release

this

afternoon. This relates to an error that may require a fourth quarter adjustment

to earnings on the order of $0.15 per unit, however, substantial recovery

of the

cost of this error is anticipated. I’ll have more on this later.

Having

covered the highlights for the quarter, I’ll now give you a more detailed

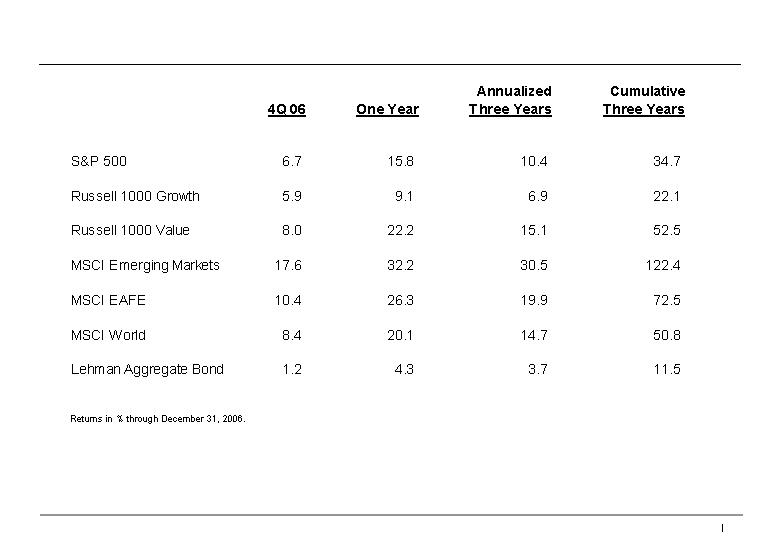

description of our results. As shown on display four, you’ll see that all four

U.S. capital market indices were up significantly for the second consecutive

quarter, with the equity indices posting their best quarter of the year,

and by

the way, their strongest year since 2003. Moreover, the S&P 500’s gain of

15.8 percent was more than 500 basis points ahead of its 15 year

average.

On

display five, you’ll see that non-U.S. capital markets, as represented by the

three MSCI indices, also had an outstanding quarter and year. MSCI Emerging

Markets and MSCI EAFE more than doubled their impressive third quarter returns

and, more importantly, the 12 month returns for all three indices were

spectacular, ranging from 20.1 percent to 32.2 percent. The MSCI EAFE and

MSCI

World indices each recorded their best annual returns since 2003.

Meanwhile

relative returns for our clients for the quarter and, more importantly, for

the

one, three and five year periods in our Value Equity services were extremely

strong, and in some cases, outstanding. This is particularly true in our

global

and international service for institutional and individual clients alike

with

returns as high as 840 basis points higher than respective benchmarks, or

Lipper

averages.

Our

Fixed

Income services have generally done well, in some cases substantially so,

performing above benchmarks for our institutional clients and above Lipper

averages for our individual clients. More importantly, we’re seeing continuing

improvement in the relative performance numbers in our Fixed Income services,

as

investments in research, analytical tools, and portfolio construction are

benefiting our clients.

In

contrast, our relative performance in our Growth services was weak for the

year,

especially in the U.S. With that said, the valuation compression between

the

value and growth components of the capital markets has reached a point where

continued underperformance by growth appears unlikely. We believe our Growth

Services are well positioned to benefit from this change in trend.

With

the

review of absolute and relative market returns as the backdrop, let’s turn to

display seven for a summary analysis of assets on the management by distribution

channel for the three months ended December 31, 2006.

As

you

can see, market appreciation, coupled with strong net asset inflows, resulted

in

AUM growth of 8.7 percent. Net flows for the quarter were approximately $10.6

billion consisting of $6.3 billion in Institutional Investments, over $2.3

billion in Retail, and nearly $2 billion in our Private Client

channel.

Display

eight shows changes in assets under management by channel for the 12 months

ended December 31, 2006. Our AUM increased approximately $138 billion, or

23.9

percent for the year. Net inflows were strong, totaling $47.8 billion for

an

organic growth rate of 8.3 percent, and investment performance added $90.1

billion, or 15.6 percent.

Record

gross sales of over $112.5 billion for the year were nearly 40 percent higher

than 2005’s gross sales. Each channel posted a new record for gross inflows for

a calendar year, with Institutional Investments totaling $53.8 billion, Retail,

$44.3 billion and Private Client, $14.4 billion. Net inflows by channel consists

of approximately $27.2 billion in Institutional Investments, $12.2 billion

in

Retail and $8.4 billion in our Private Client channel.

Turning

to display nine, we have the summary of changes in AUM by Investment Service

for

the three months ended December 31. Our Value Equity service was clearly

the

main driver of total inflows for the quarter, with record net inflows of

$10.2

billion. Fixed income had $1.6 billion in net inflows, while our Growth services

were essentially flat.

Turning

to display ten, you see for the 12 months ended December 31, Value Equities

again led the way with about $54.8 billion in gross sales, and $31.5 billion

in

net inflows, both new firm records.

2

In

addition, market appreciation of our Value Equity services was nearly $65

billion for a total increase of over $96 billion, or 40.5 percent in 12 months.

Gross inflows for growth equities were almost $34 billion, with $13.8 billion

of

net inflows.

Fixed

income services achieved net inflows of $6.8 billion compared to no net flows

in

2005. With our improving relative performance in fixed income services, we

expect Fixed Income net flows to increase still more in 2007.

Let’s

turn to display 11 where I start my discussion of our distribution highlights

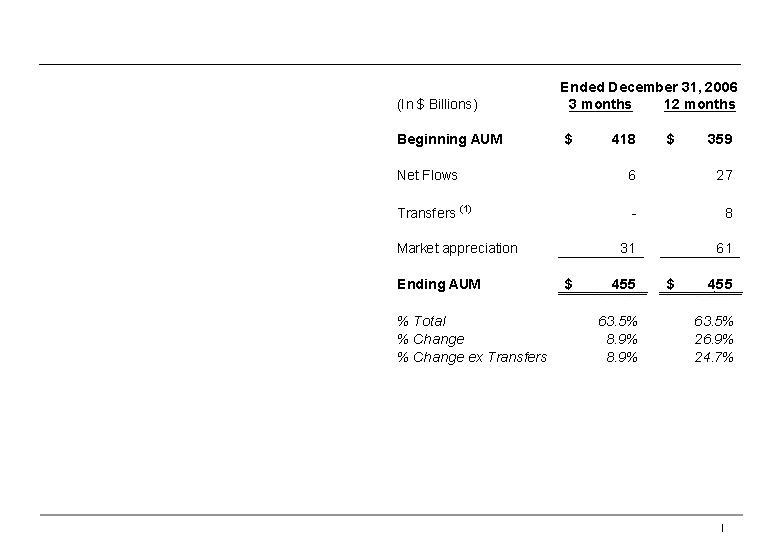

beginning with our Institutional Investments channel. At December 31, our

Institutional assets totaled $455 billion, or 63.5 percent of our overall

AUM.

The

8.9

percent increase in institutional investments AUM for the quarter was primarily

driven by market appreciation of $31 billion, while net inflows were about

$6

billion as we funded 140 institutional mandates.

During

the fourth quarter, our Value Equity and Blend Strategies services accounted

for

roughly 70 percent of all new assets. Now looking at it from another way,

global

and international services comprised approximately 75 percent of all new

assets

in the quarter, a continuing trend. And lastly, our pipeline of won but unfunded

new institutional mandates remains strong.

Turning

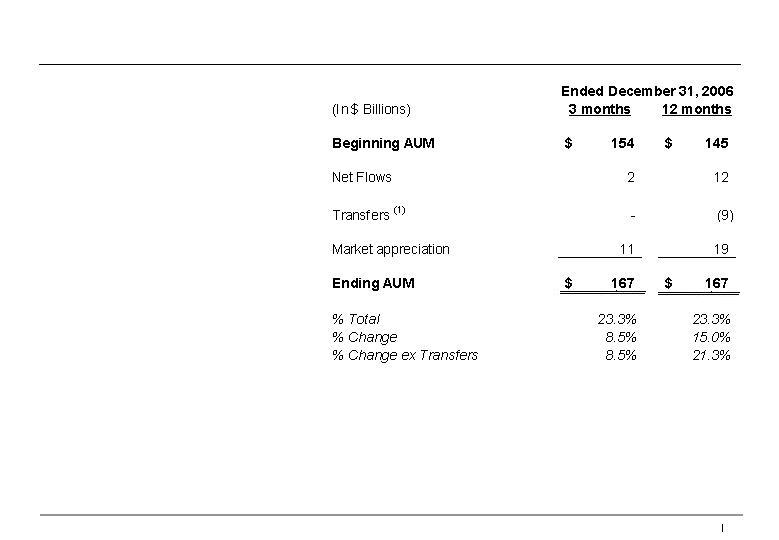

to display 12, you’ll see that our Retail assets under management are up $13

billion, or 8.5 percent, for the quarter, to $167 billion, and represent

23.3

percent of our total AUM.

As

you

can see, market appreciation accounted for most of the increase in the quarter.

For the full year, net inflows were $12 billion, an organic growth rate of

8.4

percent, which is up, which was our best year since 2000 and compares to

only

$1.1 billion of net inflows in 2005.

The

organic growth came from significant increases in Global, International and

Multi Strategy services. The net flows were across both Equity and Fixed

Income

services and in both our U.S. and Luxembourg funds. Oh yes, 2006 marked the

first year of positive net sales for U.S. retail mutual funds since 2001

and the

sixth straight consecutive quarter for net flows for the channel.

Display

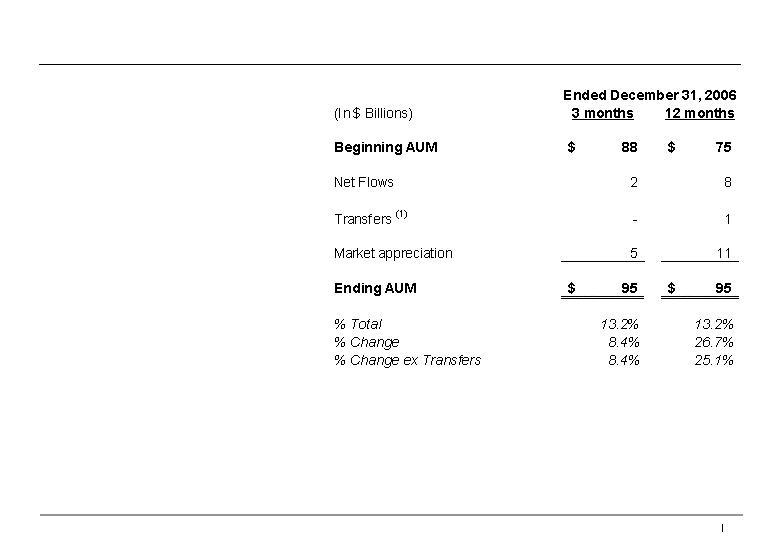

13 shows our Private Client channel highlights. Here you can see that the

assets

of our high net worth clients represent 13.2 percent of our total AUM, as

total

AUM grew by almost 27 percent year- over- year to $95 billion, mostly the

result

of market appreciation and double digit organic growth for the year.

We

continued to invest in our Private Client business as we added 37 financial

advisors, for a total of 298, a 14.2 percent increase over the past 12 months.

Highlights

for Institutional Research Services are shown on display 14. Revenues totaled

$89 million for the quarter, a 1.9 percent increase from a year ago, driven

primarily by European business. However, as shown in the appendix on display

37,

after adjusting for a reclassification of transaction charges associated

with

investment management clients, research revenues actually increased by 6.1

percent versus the prior year quarter and 16.2 percent for the year.

Our

market share improved in the U.S., thanks to strong growth in algorithmic

trading volumes and increased acceptance of our research services. These

gains

were partially offset by pricing pressure and a shift in mix to trading services

having lower revenue yields. Full year revenue grew strongly in our London

based

operations as well, with the fourth quarter run rate recovering from some

weakness in the third quarter.

Also,

during the quarter Institutional Investor released results of their “Best U.S.

Independents” survey, and our performance was excellent. Our analysts ranked in

26 sectors, including 23 first place finishes in the survey.

In

summary, we’re quite pleased with our results for the fourth quarter and the

full year for all four of our channels. The success and continued dedication

to

improving our level of service across all of our distribution channels, coupled

with outstanding performance of our investment services, will further our

progress toward achieving our goal of becoming the most admired investment

firm.

3

Before

I

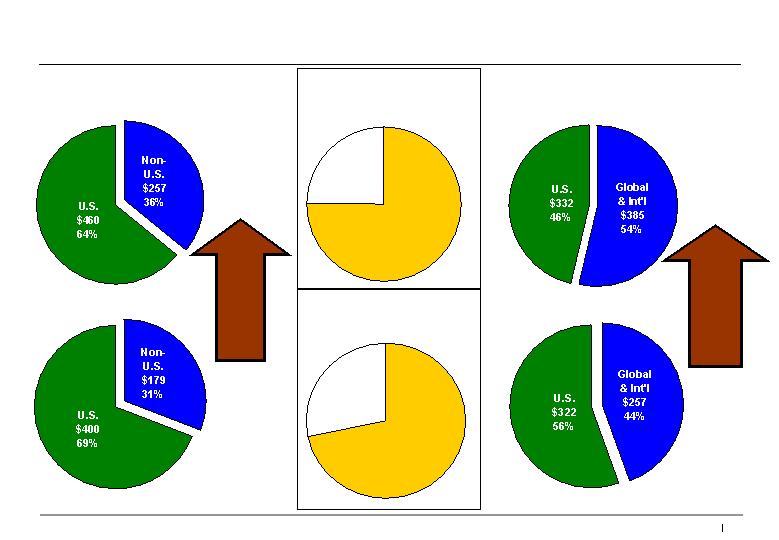

begin my review of financial results, I’d like to highlight the diversity of our

assets under management. Turning to the center pair of pie charts on display

15,

you can see that we currently have 75 percent of our $717 billion of total

AUM

in Equities, versus 72 percent a year ago, and manage $177 billion in Fixed

Income securities.

Looking

at the two other sets of pie charts, you’ll note that our firm’s business

continues to become increasingly global from a client domicile and investment

service perspective. The pair of pie charts on the left side of the display

shows that AUM of our non-U.S. domicile clients increased by 44 percent from

December 2005 to $257 billion, compared to the 24 percent increase in total

AUM.

The

right

side of the display illustrates that over the past 12 months our assets in

global and international investment services grew by 50 percent, from $257

billion to $385 billion, resulting in Global and International services now

accounting for 54 percent of the firm’s total assets under management, compared

to just 44 percent just one year ago.

And

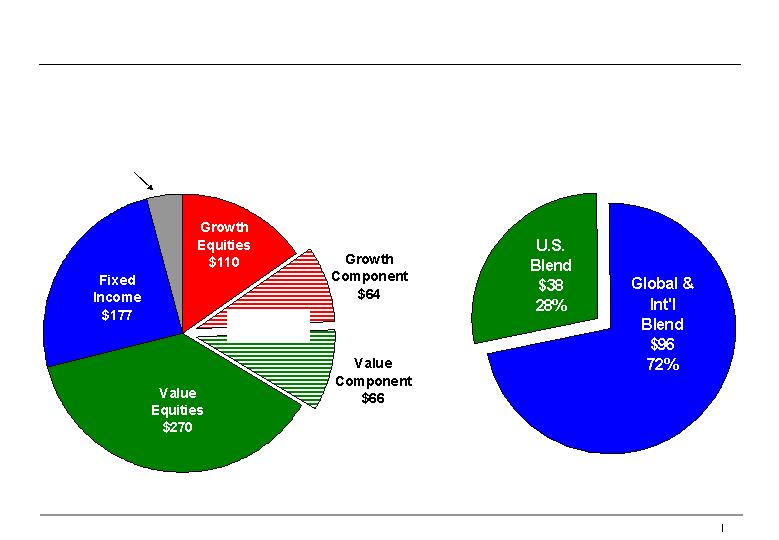

finally the pie charts on display 16 highlight the diversity of our investment

services and the growing importance of our Blend Strategies services. Our

Blend

services, which are offered in U.S., non U.S. and global constructions, totaled

$134 billion at quarter end, and are up 52 percent versus 2005.

Now

that

I’ve provided some highlights of the capital markets and our performance, asset

growth, key trends in our distribution channels, and the diversity and changing

nature of our asset mix, let’s turn to our firm’s financial results, starting on

display 17.

Net

revenues for the quarter increased 30.3 percent to approximately $1.2 billion,

a

record for the firm, compared to $911 million in the fourth quarter of 2005.

Investment advisory fees increased by 34.1 percent, or $227 million, which

represents 82 percent of the increase in net revenue.

So

let’s

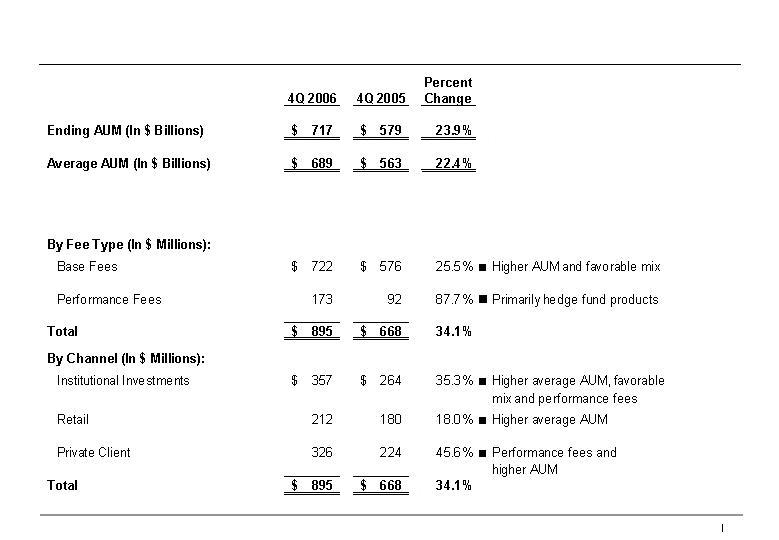

turn to display 18 where we provide additional detail on advisory fees. Here

you

can see base fees were up 25.5 percent or $146 million, versus the prior

quarter, to $722 million. The increase was primarily attributable to higher

average AUM in all three channels, but also to a favorable mix shift to more

value-added, higher-priced investment services. That is, a shift to more

equities, more non-U.S. investment services as well as growth in our Alternative

Investment services.

This

shift manifests itself with higher average fee realizations under investment

services. Another view is to consider the impact as additive to the firm’s

organic growth -- the eight percent rate as measured by cash flows becomes

double digits with respect to base fee revenues when mix shift is included

in

the calculation.

Moving

down to the performance fee line, you can see our firm’s record setting total of

$173 million for the quarter, up $87.7 percent versus the fourth quarter

of

2005. The increase in performance fees represents more than 29 percent of

the

year-over-year increase in net quarterly revenues.

Although

largely hedge fund related, our long-only services accounted for approximately

one third of our performance fees for the year. Performance fees represent

more

than 19 percent of our advisory fees in the quarter, compared to less than

14

percent in the fourth quarter of 2005.

As

our

percent of AUM with performance fees grows, revenue and earning’s seasonality

and volatility may become more pronounced as performance fees amplify the

impact

of investment returns.

With

that

said, though, the $236 million in performance fees for the year represents

just

six percent of our revenues, versus four percent in 2005, and provides us

with

the opportunity to earn significant incremental fees when we deliver for

our

clients.

Moving

to

the lower half of the display, we show advisory fees by distribution channel.

Here you can see the 35.3 percent increase in our Institutional Investments

channel, where higher AUM, a favorable mix change, and performance fees all

contributed to the revenue increase.

4

In

the

Retail channel advisory fees increased 18 percent, benefiting from higher

average AUM during the quarter. While in our Private Client channel, fees

grew

45.6 percent, driven primarily by hedge fund performance fees and higher

AUM, in

that order.

Now,

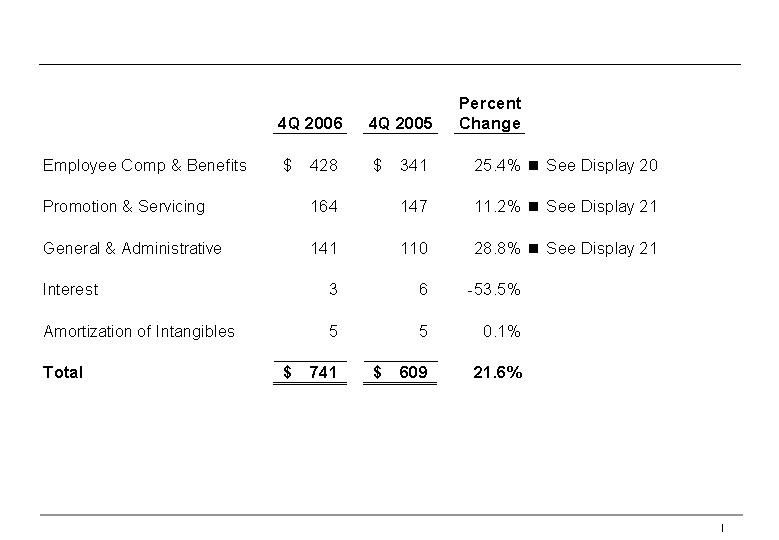

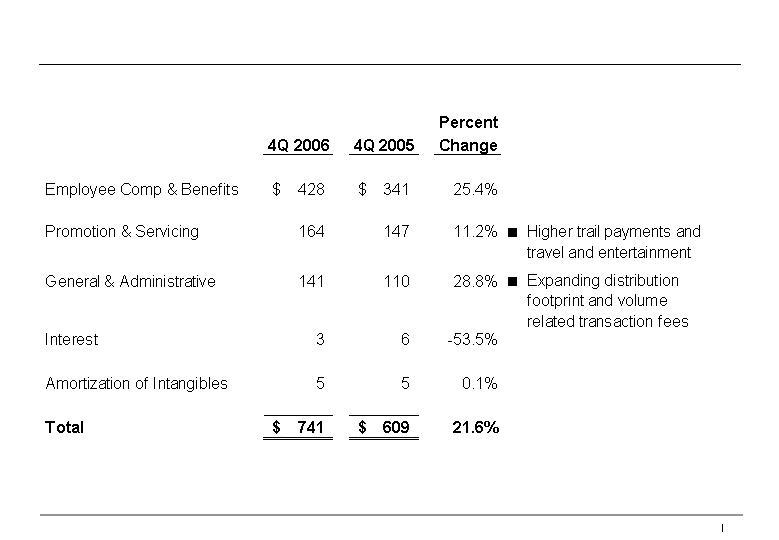

let’s turn to expenses which are summarized on display 19. The 21.6 percent

growth in operating expenses for the quarter is significantly lower than

the

30.3 percent increase in net revenues and resulted in a 450 basis point

improvement in our operating margin in the quarter.

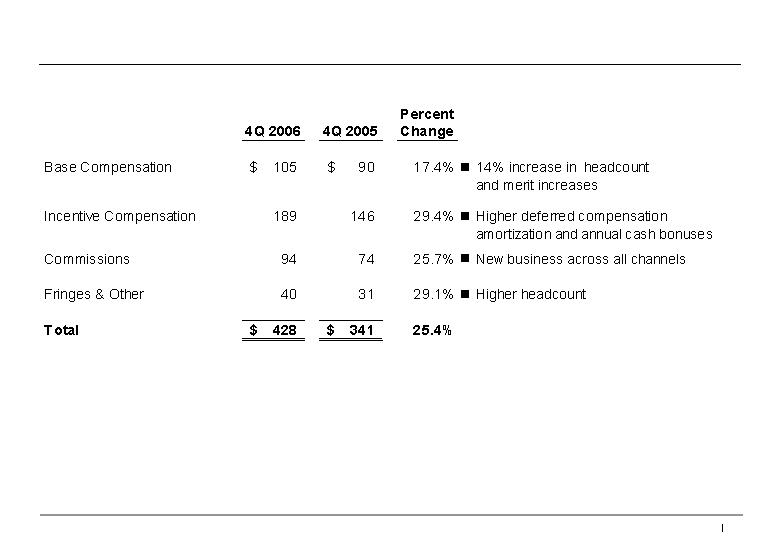

Display

20 provides additional detail on Employee Compensation and Benefits. The

25.4

percent, or $87 million, increase to Employee Compensation and Benefits

represents almost two thirds of the increase in total operating expenses

versus

the fourth quarter of 2005. Base compensation is up 17.4 percent versus last

year as we increased head count by 14 percent, or more than 600 staff members,

to 4,914 at year end.

As

I

mentioned last quarter we have increased head count in operations in response

to

the growth in volume and the increasingly complex, global nature of our firm.

Additionally, in our Retail channel we’re investing to expand distribution

capacity in the U.S. and our infrastructure outside the U.S.

In

our

Private Client channel we continue to increase our global Financial Advisor

staff levels and we’re also investing in operations and technology to support

the expansion of our platform and improve operational functionality and

efficiency.

The

increase in the Incentive Compensation of 29.4 percent, which is significantly

less than our 48 percent operating earnings increase, is attributable to

an

increase in Deferred Compensation and higher earnings, which drives annual

cash

bonuses.

Commission

Expenses increased 25.7 percent, with increases in all distribution channels.

We

should remember that growth in commission expense is actually a leading

indicator for future revenue and earnings because the full impact of new

business isn’t reflected in the current P&L, since commission schedules are

generally front loaded in the first year of the sale.

Turning

to display 21, please note that our Promotion and Servicing line includes

the

Amortization of Deferred Sales Commission, which, as shown in this afternoon’s

press release, was $28.7 million for the fourth quarter.

I’d

like

to point out that the $28.7 million includes a cumulative catch up adjustment

of

a prior period amortization that increased the expense by approximately $4

million. So considering the impact of this adjustment, you’ll arrive at a more

appropriate run rate for at least the next few quarters.

Also

on

display 21 you can see the G&A increase of $31 million, or 28.8 percent.

Expanded space in New York City and several U.S. Private Client offices,

as well

as new offices in London, Shanghai and Hong Kong accounted for approximately

one

third of this increase, while volume related transaction costs accounted

for

another third.

As

I wrap

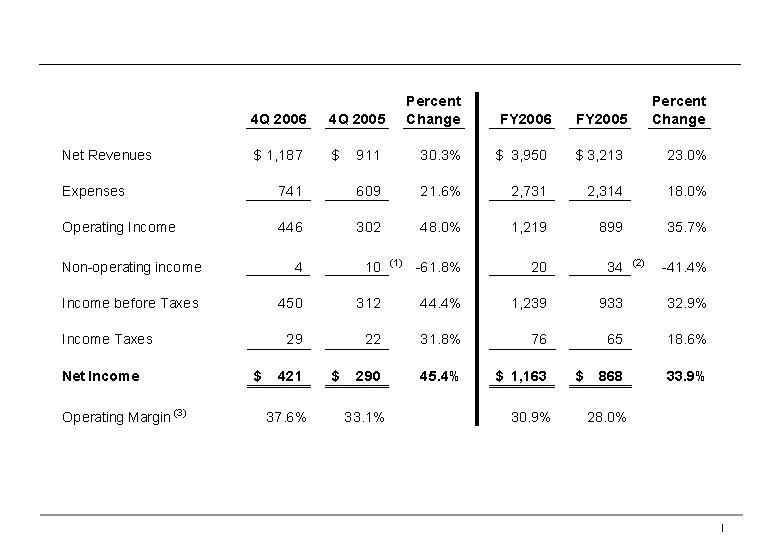

up my comments, please turn to display 22 where we present a summarized income

statement for AllianceBernstein for both the quarter and the full year periods.

Operating margins expanded by 450 basis points for 37.6 percent for the quarter

and 290 basis points for 30.9 percent for the year.

Margins

benefited significantly from the increase in performance service fee revenues

in

both the fourth quarter and the full year and a moderation in our cash incentive

compensation growth rate.

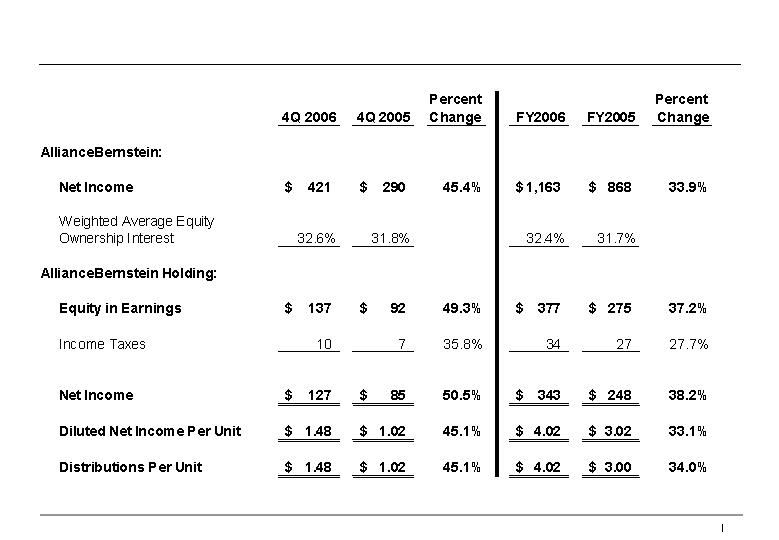

Carrying

the Operating Partnership’s fourth quarter and full year Net Income forward to

display 23, we show that AllianceBernstein’s Holding’s financial results.